We would like to think of life insurance agents as trusted advisers whose only aim is to get us the right coverage.

But the nature of life insurance -– and the job of life insurance agents -– makes them something close to our natural enemy.

Life Insurance Agent Secrets

One easy way to prevent being taken advantage of is to find an independent agent. “Independent agents save you time and money,” said Chris Huntley, co-founder of JRCInsuranceGroup.com.

“Rather than completing applications and medical exams with 15 of the best life insurance companies to see which one will approve you at the best rating, make one call to a qualified independent agent, who can place you with the most appropriate carrier based on your unique personal and medical history.”

In a lot of ways, what hurts us as consumers of life insurance actually benefits life insurance agents. Here are nine examples of what I’m talking about in a quick Life Insurance 101 article!

Table of Contents

1. Their Income Is 100% Commission

Any time you’re buying from a person compensated 100 percent by commission, your radar needs to be up and in perfect working order. Being on commission doesn’t make a person evil. But it may change his or her perspective, as well as the type and degree of products that you will be introduced to.

If the agent is entirely on commission, he or she will then have a vested personal interest in selling you products that will result in you paying the highest premium possible and hence yielding the highest commission. It is also why when you fill out the form for an online life insurance quote engine you will frequently get calls from multiple agents within minutes of hitting submit. Each one is trying to reach you first so that they can get the sale.

2. You May Very Well Be Over-Insured

Whenever an agent evaluates how much life insurance you need to have, he will almost inevitably start with numbers that are larger than anything you’d ever imagine that you would need.

For example, it’s not unlikely that the agent will suggest that you need to have life insurance equal to 30 times your annual income. If you are earning $100,000 per year, he may suggest — without flinching — that you will be adequately insured by a $3 million dollar insurance policy.

After all, you will need to provide income for your family for the next 20 years, a college education for your children, the payoff of your mortgage, and a comfortable retirement for your spouse.

He knows that it is unlikely that you will take a life insurance policy that large, but it’s an excellent starting point — for him. After all, if he suggests $3 million but walks out of your house with an application for a $1 million policy, he wins. That’s because he knew going in the door that you probably only wanted a policy for a couple hundred thousand dollars.

And you’d probably be right. After all, if you have other investments and your spouse is also well-employed, you will only need a fraction of the life insurance coverage that the agent will suggest.

Most often, life insurance is only needed to settle final arrangements, medical bills, outstanding debts, and maybe a few years of living expenses. Providing for your loved ones to live in luxury for the rest of their lives is an expense you can’t afford, or need.

3. Whole Life Isn’t a Good Investment — Or Even Good Insurance

Life insurance agents like to sell whole life insurance as the best of both worlds–- an investment program with life insurance coverage. In truth, it doesn’t do either particularly well. The insurance benefit will be limited because the premiums are high. And since so much of the premium goes to pay for investment fees and the life insurance coverage, there is relatively little left over for investment within the plan.

4. The Cash Value of Whole Life Won’t Benefit You for Years

Life insurance agents like to hawk the virtues of the cash value build-up in a whole life insurance policy. This is another myth. As a rule, it will take at least five years before you will have a cash value that is equivalent to the amount of money you paid in premiums into the policy. And maybe not even then.

5. “Buy Term and Invest the Difference” Really Is a Better Strategy

There is probably no slogan confronted by life insurance agents that is more irritating to them than this one. And that’s because the slogan is true.

Since term insurance is so much less expensive than whole life, you can buy a lot more of it -– in fact a more reasonable amount for your needs. And the investment performance of mutual funds -– particularly index funds –- dramatically outperforms that of any insurance-related investment vehicle.

Even if the combination of term life insurance and investment in a mutual fund is no less expensive than a whole life insurance premium, the money you will accumulate in the mutual fund — and the speed at which you will do it — make it a far superior investment to a whole life insurance policy. And you’ll have a whole lot more life insurance coverage along the way.

6. We Don’t Know About the Value of Long-term Care Insurance

From a consumer standpoint, there are two fundamental problems with long-term care insurance coverage:

- It’s very expensive.

- It’s not certain that you will ever need it.

Since people are living longer than ever, making a provision for long-term care has become a hot topic. Insurance agents know this, and they’re exploiting the fear.

Emotions aside, most people don’t need long-term care. And even if they do, it’s often for a short period just before death. If there are other assets available, particularly retirement assets or a home with substantial equity, long-term care insurance may be unnecessary.

And if it isn’t ever needed, you will have spent tens of thousands of dollars over many decades funding an insurance policy that was never necessary. This is an important consideration when there are so many other priorities in your household budget.

7. Your Kids Don’t Really Need Life Insurance

Life insurance agents love to sell whole or universal life insurance policies to parents of young children, stressing the advantages of the investment provisions of the policies. Those provisions, they argue, will help parents to provide funds for their children’s college educations. But nowhere is the advice of “by term and invest the difference” more relevant.

You should have only enough insurance coverage for your children to pay for final expenses and uncovered medical costs. In most cases, a $50,000 term life insurance policy will get that job done with money to spare. There is no need to replace lost wages with a ridiculously large policy.

And as we’ve already discussed, insurance-related investment vehicles are underperforming investments. You’ll be far better off investing money in a mutual fund for your children.

8. There Is No FDIC Equivalent Back-Stopping Insurance Companies

This is a very relevant question – but seldom asked — since life insurance agents like to position themselves as investment advisers. The investments that they sell are almost always exclusively insurance products. However, there is no equivalent to the Federal Deposit Insurance Corp. that will back up the life insurance company in the event of investment failure.

There are arrangements within each state for companies to collectively back a failed insurance company, but there is no apparatus in place to deal with a systemic failure such as the financial meltdown that hit the banks and financial companies a few years ago.

While this has obvious implications for the life insurance coverage that you pay for and expect to have, it becomes much more significant when you have a lot of money sitting in insurer-sponsored investments.

Life Insurance Agent Secrets

| SECRET | DESCRIPTION |

|---|---|

| 100% Commission Income | Agents Are Motivated by Commissions, Affecting Their Recommendations |

| Potential Over-Insurance | Agents Often Advise Excessive Coverage, Leading To Higher Costs |

| Whole Life Limitations | Whole Life May Not Excel as an Investment or Insurance Due to Costs |

| Delayed Cash Value Benefits | Cash Value in Whole Life Takes Time to Accumulate and Benefit You |

| “Buy Term and Invest” is Better | Term Insurance With Investing Can Outperform Whole Life Policies |

| Uncertain Value of Long-term Care | Long-Term Care Insurance Can Be Costly and Unnecessary for Many |

| Children May Not Need Life Insurance | Minimal Coverage Is Often Sufficient for Children, Not Excessive |

| No FDIC Equivalent for Insurance | Insurance Lacks FDIC-Like Protection, Impacting Investments’ Safety |

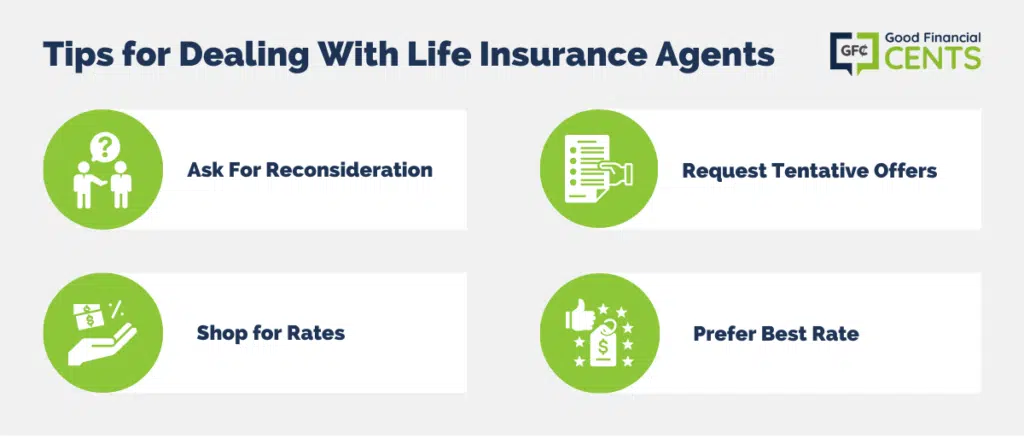

More Tips for Dealing With Life Insurance Agents

If you apply for life insurance, keep these four tips in mind from Jeff Root, a life insurance agent and founder of Rootfin.com. And again, they’re not tips your agent will be likely to recommend.

- If You’re Not Satisfied, Ask For Reconsideration: Life insurance underwriters will always offer the best possible rate class as permitted by their underwriting guidelines; however, if you’re not happy with the life insurance company’s offer, your agent can submit a “reconsideration request” and ask the underwriter for a better offer. Most agents don’t even mention this as an alternative because of the extra work involved in drafting a letter convincing the underwriter why they should qualify for a better health classification.

- Ask For Tentative Offers: Consumers can get “tentative offers” from life insurance companies before applying for life insurance. Independent life insurance agents send your risk anonymously to various underwriting desks. Underwriters typically reply within 48 hours with a health classification in what we call a “tentative offer”.

You can attach this tentative offer to the life insurance application, and the company you apply with must give you this rate unless you withhold any information from them. This is a must for people with health issues applying for life insurance.

- Shopping Won’t Necessarily Get You a Better Rate: Going from website to website won’t result in finding better rates. However, each company looks at your health differently. It’s your agent’s job to fit your unique health situation into the underwriting guidelines of each company and then see who provides the best rates.

- Most Applicants Won’t Get the Preferred Best Rate: Less than 5 percent of people who apply for life insurance can qualify for “preferred best.” Yet it’s the No. 1 health classification quoted on websites.

Final Thoughts – Secrets Your Life Insurance Agent Might Be Keeping

When dealing with life insurance agents, consider these key points. Opt for independent agents who can save you time and money by connecting you with the right insurer. Beware of agents working on commission, as their interests may lean toward higher premiums.

Agents often recommend excessive coverage levels. Whole life insurance may not be the best investment due to high costs. “Buy Term and Invest the Difference” is a more cost-effective strategy. Long-term care insurance isn’t necessary for everyone. Minimal coverage suffices for children.

You are on point. We had two visits recently and it was a HORRIBLE experience and you confirmed everything that we were experiencing and what we knew to be true. Thank you for that confirmation that we made the right decisions. We couldn’t get this guy to leave without being rude. It was 2 hrs of ugly.

You sound like a real Dildo and look like one too. You financial advisors as you call yourselves are real thieves and mindless creeps. I hope no poor soul believes any of your lies!

You sound like a total idiot and a stroke. Do you think that throwing these agents under the bus is going to give you some sort of credibility? You are probably so used to screwing and lying to consumers you think they are all liars and thieves just like you. Financial Planners are usually snakes and leeches who con old people into investing in some garbage that pays you the highest commission. You should re-name your website www.horseshitfinancialcents.com.

I don’t listen to critics by the name of “Vernon”. Know what I mean Vern?

I’m not in the industry and these opinions are the most horrible statements ever! This is terrible advice for people. The one the struck me the most is kids definitely need life insurance! No exam is required for children under 18yrs old. So they have a milllion dollar pppolicy for the rest of their lives paying $10/month for. That’s better than waiting until you’re 40 and paying $300/month for that same policy. The idiocy of this entire article!!! I hope ppl don’t believe this!!!

This is an incredibly wrong and biased article. The historical data, facts and statistics on the benefits of Whole Life Insurance absolutely diminishes your argument and opinion. First, and foremost, your use of the word “investment” when it comes to Whole Life is deceptive and inaccurate. Whole Life, Term and Universal Life are financial instruments and NOT investments or investment tools. While Whole Life is most definitely an Asset Class, it is undoubtedly and most assuredly Life Insurance. Term, Whole Life and Universal all have their respective and beneficial places and uses. To knock one to suggest your own flawed opinion of “buy term and invest the difference,” a strategy that only sounds and works good in theory, displays your persuasion in being more toward investing, something with risk, something which can be lost completely. The absolute opposite of what insurance does, which indemnifies and guards against risk. This is a very poor article.

This is obviously wrote by a financial advisor. You should sit down with both to decide what is best for you. Each professional has a different view on Financial planning. If you are not insuring your liabilities, than you are being lead down a rabbit hole.

The bottom line is buy term invest the difference it good for some people but not for all. If everyone used this strategy, then no one would ever lose money in the stock market. But we all know that the market goes up and down and most people are not disciplined enough to go thru the up and down.

It is funny how Financial advisors state Life Insurance agents are get paid on commission. Financial advisors get paid on commission as well. Can any financial advisors guarantee that you will live to meet your financial goal? No they cant.

Do your research when investing in a stock portfolio and Life insurance products. I would sit down with an advisor that considers your present situation and the future.

Regarding Long Term care. The chances of having a long term care event is pretty high. You can pay dollar for dollar for your care or pennies on the dollar. It is expensive if you try to get it when you are older than 60. Look up how many people lose their assets to a medical issue or death.

I don’t think you should throw all your money at an expensive policy, not having anything is very foolish.

I had an agent approach me talking about retirement, he introduced me to the Index Universal Life Insurance, an insurance with cash accumulation. The return is up to 15% but honestly depends on the average of S&P 500, Im still guaranteed not to ever lose money and still make 0.75% in case the market is negative. He was really through. My question is, in terms of protection and investment was this the right product?. I just couldn’t look at term insurance giving me nothing in return and then I was afraid of losing money in the stock market. Did I make the right choice? Thoughts?

Angie,

Indexed Universal Life is a great product when set up correctly. It needs to be a minimum death benefit and a maximum funded policy in order to perform at it’s best. Remember life insurance fees are the highest in the first 5-10 years. A good agent can help keep those costs lower throughout the life of the policy.

IUL policies have beat the S&P easily since 2000. Why risk money in the market when safer strategies are performing better? Plus, with the ability to take tax free loans and most policies have chronic, critical and terminal illness riders built in. No portfolio can compete with that. Angie, stay the course, fund it to the max that the policy will allow and enjoy the benefits. Smart purchase

My husband and I have a whole life and a term life policies for about 15 years but we are not happy any longer with the insurance company (Farmers). The polices are underwritten by another company. Can we break with Farmers and work directly with the underwriters? We want to go to another insurance company but want to keep my life insurance policies intact since I have had them for so long. How do I do that and is it even worth doing so? I will be changing the insurance company for car and home owners. The term is 30 years and the whole life has a cash accumulation but it isn’t much in either whole life policy. After reading your article it looks like we got “suckered” into the whole life buy. *sigh* Any help would be appreciated.

@Valerie Yes, you should be able to do that. I would contact the underwriters to see what they suggest your best options are.

Hi, I read your comment and agree with 100%. I am an insurance agent and read through your post. I didn’t get offended, because I’m not one of those people that try to make a lot of money off of people. I effortlessly search for the best deal for clients and get them pre-approved with underwriting by talking on the phone with underwriting in front of them with the carriers I had in mind. I email or mail out cheap quotes and cheap final expense to people, but no one wants it. So I find that I am on the people’s side and they still turn me down 30% of the time. Might be because of other agents or they look at it as a benefit that they will never see so why get it? I tell them the reason and they still think life insurance is a waste of money. Life insurance needs a new facial and working body of parts.

Hi Stephen – What you’re saying has a lot of truth to it. Let’s face it, people are a lot more concerned with preparing for their retirement, not their death. It’s not a happy subject! But retirement is a major selling point for life insurance because it kind of dovetails in. I mean if you’re talking about retirement, you can’t help but move into estate planning, and that’s where life insurance becomes an easier sell (what are they going to leave their kids, paying estate taxes, etc.). But apart from that, you’re right. Unless they recently had someone close to them die, it can be hard to make a case for life insurance, especially if they have a policy through work.