As a child, my mom and stepdad would take me on RV trips all across northern California and Nevada during the summer.

I remember it being some of the best memories of my childhood. I knew that when I got older that an RV trip was in store for the Rose family. I just didn’t realize it would come this soon…..

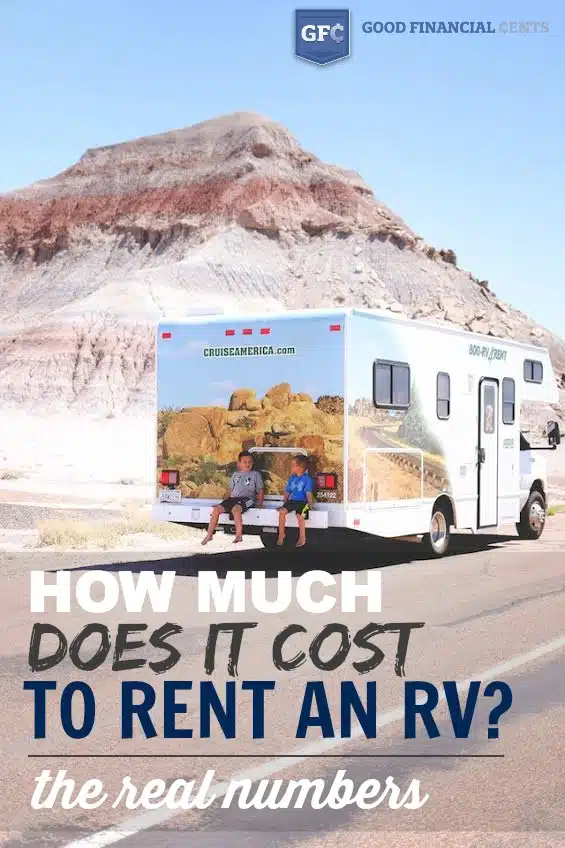

A few summers ago, the five of us hopped into a rented RV for 14 days, with the only planned destination being the Grand Canyon.

Everything else was meant to be an adventure, and it sure was.

Many people were asking me questions about what it takes to rent an RV and how much it costs, so I knew that I had to do a recap post on it.

So if you’re ready to join me and Cousin Eddie and go off on your own RV adventure, here’s what you need to know…

“That There’s an RV” – Cousin Eddie, Christmas Vacation

Table of Contents

10 Things You Must Know Before Your 1st RV Trip

1. Where Do You Rent an RV?

Great question, because I had no idea either. The first place I went to do research is where everybody does a lot of research nowadays: Facebook. I asked on Facebook where is a good place to rent an RV. I had a few people in my area suggest a local RV dealer. Perfect.

I called them, and on my first attempt, I got an answering machine. Hmmm. Trying to figure out why a business in the 21st century doesn’t offer a live person to talk to. That’s okay. I live in southern Illinois. I get it. I left a message telling them I’m very interested in renting an RV, please get back to me as early as possible.

A day goes by. Another day goes by. A week goes by. Another week goes by.

Nothing. I still have plenty of time before I want to rent the RV, so I thought, “What the heck, I’ll give it a try again.”

I call again. Guess what? Answering machine. Really? I left another message explaining that I called a few weeks ago, was still interested in renting an RV, and I’d love for somebody to get back to me.

Time goes on, and I get busy with other things, forget about it, and realize that another few weeks have gone by. I once again share on my Facebook profile: how many chances would you give a business to get back to you? I think I updated the comment to the same feed, seeing what the people would say that they knew and had rented from this dealer before.

Once again, I got positive feedback that they had great experiences with the individual; not sure what’s going on, but to give it one more shot. Reluctantly, I agreed. I called back a third time and finally got a chance to talk to somebody who I think is the owner.

I talked to the guy for about 10 minutes, telling him what I wanted. He says he’s busy at the moment, but he’ll get back to me with some information by the end of the week. At the end of the week comes nothing. Monday rolls around. Nothing. Tuesday rolls around. Nothing.

At this point, I’m done. I immediately go to Google and type in “Rent an RV,” and I come across Cruise America. I read a few reviews, and it seems like what I’m looking for. This is perfect.

I call the toll-free number, and guess what happens? I get to talk to somebody. Immediately. I tell them what I’m looking for, and they explain everything in great detail.

I’m taking notes, writing down numbers, and I’m excited. I’m actually making progress. I tell them the time frame of when I’m looking to rent the RV, and they tell me that starting in June is their peak season, and that’s when prices go up.

If I’m able to reserve the RV and actually begin the rental in May, then I would get a lower price and save money. It worked out perfectly since my oldest son would be done with school on Friday, May 30.

I agreed to pick it up on May 31. At this point in time, all I have to do is put down a $300 reservation deposit. Since I’m gung ho on the idea of renting the RV, I go ahead and lock it in, and I can’t wait to share with my wife the exciting news.

2. How Much Does it Cost to Rent an RV?

According to Cruise America, the cost of renting an RV depends on the following factors:

- The cost per night the rental company charges. During peak vacation months such as July and August, those nightly rates can vary.

- Then you figure out how many miles your trip will take. Most RV rental companies charge a certain amount per mile. That’s from 35 to 50 cents per mile.

- You’ll then multiply the number of nights you’ll be renting the RV by the nightly rate and add that to the mileage times the cost per mile. For example, if the nightly rental rate is $99 and the total mileage traveled at, say, 35 cents per mile, a five-night, 500-mile trip would be $670.

- Most RVs come with a generator, so there is a relatively small charge associated with the generator. During warmer months, generator use will increase as the onboard air conditioner is used more.

- In determining how much it costs to rent an RV, you should also consider the cost of kitchen utensils (pots, pans, etc.) and bedding. If the RV rental company provides those items, there will be a fee; however, you usually have the option of bringing your own utensils and bedding. In that case, of course, there is no fee charged for those items.

At the time we rented our RV, here was our estimated cost:

- 14 Nights: $938.00

- 3000 Miles: $1020.00

- State Tax 5%: $97.90

- Total Miles Included With Rental: 3000 miles

- Total Charge: $2055.90

- Security Deposit: $500.00

- Less Reservation Deposit: $300.00

- Balance Due on Pickup: $2255.90

Below is the confirmation email that I received from Cruise America that explains their refund policy as well as some additional costs.

- Your down payment is fully refundable up until close of business 7 days prior to travel or if booking within a week of travel on close of business on the day booked.

- Pickup time at our locations is 1-4 PM, and drop off time is 9-11 AM (Saturdays the times can be different).

- We do require a security deposit of $500.00, separate from the rental cost. This comes back to you at the end of the trip as long as the vehicle comes back in the same shape you picked it up in. We also refund unused miles that were prepaid in the reservation.

- Generator use fees are $3.50 per hour. Most people using generators for their electricity average about 2 hours per day. If you are plugging in at a campground or other area, you will not need the generator for electric use.

- Insurance for drivers 25 and older and 24-Hour Travelers assistance is included in the rental price.

- Please call the location a few days ahead of time to arrange your pick-up appointment.

Rates include all taxes and travel assistance. Cruise America rentals are covered by free insurance with a $1,500 deductible policy. For additional coverage, you can upgrade to their Zero Deductible policy.

It was comforting to find out that I didn’t need any additional RV insurance or auto insurance coverage!

According to Google Maps, hitting the Grand Canyon and back would be roughly about 3000 miles. I probably should have guestimated that we would use it more, but I thought that was a safe play. Turns out that we actually traveled 3440 miles.

At .34 cents a mile, that was an additional $149.60. Not great, but really not that bad. We opted to buy the kitchen set, which included a skillet, pots, pans, plates, bowls, silverware, et cetera.

That was an additional $100, and the reality is that we didn’t need it. We never cooked in the RV other than using the microwave, so really, that was pointless.

Luckily, we were able to keep the set, so we brought most of the stuff home and donated the rest. Since we didn’t cook, we didn’t use a lot of propane. Actually, we only used one ounce of propane, which was $20. The reason we had to use that was that our refrigerator ran on propane, so that’s where that cost came into play.

We only used four hours on the generator, and at 3.50 an hour, that was an additional $14. Why the four hours? Typically, the only time we needed the generator was whenever the RV was really hot, and we needed the AC kicked up a bit, especially in the back. We predominantly used this in Texas and New Mexico whenever the heat was at its highest.

What About Gas?

This was the expense that I was most concerned about. I had no idea what to expect and how much I would be spending on gas. I read that RVs will get anywhere from 6 miles on the gallon up to 12 miles to the gallon, so I wasn’t all that hopeful.

We put a total of 3440 miles on the RV, needing a total of 397 gallons of gas. The average price per gallon was about $3.50, and our total fuel bill for the entire trip was $1,400.67.

Ouch.

I knew it was a lot, but I didn’t realize it would be that much. I tried to keep our gas tank above or around the halfway mark most of the time, and on average, that was about $100 to fill up. A few times, it got down to a quarter tank, which was the lowest I ever let it go, and those times, it was roughly about $150.

I couldn’t imagine making an RV trip when gas was north of $4 a gallon. The highest that we had to pay was in Williams, Arizona, at $3.89 a gallon, and the lowest that we had to pay was in Tucumcari, New Mexico, at $3.35 a gallon.

3. What About Other Costs?

In addition to gas, campground fees, generator costs, et cetera, other costs include the random stops that you want to hit while you’re traveling.

For example, we hit up a few national parks while we were driving, including the Petrified Forest in Arizona. It was $20 just to drive through there. If we hadn’t done the pink jeep tour at the Grand Canyon, it would’ve cost $25 to get into that national park.

On the way to Flagstaff, Arizona, I happened upon a sign that boasted about the largest meteor crater in the United States, and of course, I had to stop. After we drove six miles off the road in the RV, we got to the place only to find out that it was $12 a head to get in.

At that point in time, we basically felt stuck, but they did give us a military discount, so we decided to see it. I’ll tell you, I definitely think it was worth it, but these are the type of costs that you really don’t anticipate but you know will occur, especially on a road trip.

One thing I have learned is that having one of the best travel credit cards is a must-have for trips like these. When you’re forking over $3,000 or more for the rental, plus paying for everything else that pops up, it makes sense to earn something in return.

If you’re someone who travels all the time, I would probably suggest a top travel card like the Chase Sapphire Preferred® Card. With this card, you’ll earn 2X points on travel and dining, plus 1X points on everything else.

Plus, you’ll score a 50,000-point signup bonus worth $500 in cash-back or gift cards after spending just $4,000 in 90 days. This is the perfect card to get right before you take off on any journey around the country.

4. How Hard Is it to Drive?

I have driven a five-ton truck in the military, so I was comfortable driving the RV, but the five-ton was only driven in short distances, never for an extended road trip. The one thing that I was impressed by was that the RV was able to get up and go.

In Oklahoma, northern Texas, and also Arizona, the speed limit was 75, and it was easy for me to get the RV at that speed.

What I didn’t anticipate was how much the wind coming across the interstate or highway would affect the driving. It almost felt like the alignment was off because every time I would let go of the wheel, it would sway pretty hard.

After a while, I realized it was the wind that was pushing the RV, making it extremely difficult to drive. Predominantly I was driving with my hands at 10 and 2, with my hands clenched because every little wind gust I would come across would push me on the shoulder.

Things were always interesting, too, when a semi-trailer would come up and pass me on the left, creating a sort of wind vacuum that would also push the RV.

Because of this, I typically didn’t drive more than four to five hours a day, taking the necessary stops. The longest I ever drove was when we were trying to get from Colorado Springs to Topeka, Kansas. It was eight hours of driving, but it took us 12 hours to complete.

5. Where Do You Stay?

I have a lot of clients who have RVs and will travel all across the U.S. Everyone I polled about where to stay mentioned that they typically stay at KOA Campgrounds. KOA Campgrounds are kind of like the Holiday Inn of RV parks.

A majority of the ones that we stayed at always had a pool, a playground, Wi-Fi, laundry facilities, gift shops, and sometimes even food. The one in Flagstaff, Arizona, even had an Elvis Presley impersonator.

The costs there are anywhere from $35 up to $45 per evening, depending on what all hookups you need. If you just needed electricity, it was cheaper, but if you also needed sewer and water, then it would be a little bit much. We never had an issue getting to a KOA campground where they had no room available.

I could see though, that if you were near a tourist area like the Grand Canyon, it wouldn’t be a bad idea to call ahead. We stayed at the Williams, Arizona, KOA campground on a Friday evening, and that was the most packed of any of the KOAs that we stayed at ever were.

On the way back home, we met up with some of my wife’s friends who have stayed at several campgrounds before, and they wanted to stay at the Yogi Bear campground, otherwise known as Jellystone, which is located just outside St. Louis.

The campground price was just about the same as $45 per night, but it was definitely a lot more kid-friendly. The rates do vary depending on which location you are visiting, the time of year, and what you need for hookups.

They had a nice pool and a huge playground, and plenty of activities for the kids. When we checked the map for Yogi Bear Campgrounds, they are predominantly in the Midwest and East Coast rather than more on the West Coast, so we didn’t get a chance to stay in any until near the end of our trip.

The only one that we encountered was in Colorado, but we were not at a point where we were ready to stay.

6. Is It Better to Do an RV or a Camper?

At about the halfway point of the trip, I remember asking my wife, “So, what do you think is better? Taking the SUV and staying at hotels, having an SUV and towing a camper, or the RV?” We started talking about the pros and cons of each.

With the SUV/hotel idea, obviously it would be much more expensive, but you could cover the ground a whole lot faster. What would probably be the most annoying thing was the number of potty breaks that we had to take with the kids – as every parent knows, your kids are not on the same potty schedules, so there had been multiple stops having to take care of business.

Plus, with snacks and drinks, they also become annoying having to furnish our kids with those, especially if we’re trying to cover a lot of ground.

The camper would also be similar. Since you’re not allowed to ride in the camper when you tow it, you’d be subject to all the same potty breaks and snack breaks that you would with the SUV. The only benefit would be that at the campground, you’d be able to unhitch from the camper and tour some areas that wouldn’t be accessible in a camper or RV.

With the RV, our kids were able to take potty breaks when needed, and with the fridge right there, had plenty of juice and snacks whenever they wanted. This allowed us a lot of uninterrupted driving time.

Driving in traffic was definitely interesting, but it wasn’t impossible with the RV. The most annoying thing was parking. Oftentimes, we would have to park several blocks away from our destination if we were trying to eat at a local diner, but overall it wasn’t too bad.

If your plan is to stay in a national campground and never really tour, then it shouldn’t be that big a deal.

7. How Much Stuff Can You Bring?

A lot. The one annoying thing about where the RV pick-up location was is that it was 2 1/2 hours away. That means we had to load up the mini, including our extra carry-on bag that goes on top of the mini, to get everything packed up and loaded.

We were afraid that we might not have enough room in the RV, but by the time we got everything unpacked out of the mini and uploaded in the RV, we realized that we had plenty of room.

We had four full-sized suitcases, chairs, toys, food – everything that you could think of – and we still had plenty of room in the RV. Most of the bigger stuff you had to keep stored in the outside compartment of the RV, so you couldn’t access it while driving, but that never really proved to be an issue.

8. Can You Really Live in That Thing?

Ha, ha. I’m pretty sure that this was a question that my wife was wondering before we went to go pick up our new home on wheels. Since we survived the two-week RV excursion, I’m happy to say yes, you actually can live in this thing.

The 25-footer ended up being the perfect size for a family of five. The wife and I took the Queen (it felt more like a twin) bed in the rear. Our two oldest boys slept in the converter bed that was above the driver and passenger seat.

Our youngest son slept by himself on the converted bed that also served as the dining room table. He easily could have fit up top with the two older brothers, but we did have a fear that he may roll off and fall, which actually did happen to both our youngest and our middle son during the trip. Don’t worry; they’re okay.

One of the things that helped the most, at least for me going to sleep each evening, was running the air conditioning/heating unit.

Why is that? Because the noise of the unit would drown out our kids’ giggling or any other noise outside our campground.

Whenever it would shut off, you could hear absolutely anything, including our neighbors talking, and that would generally wake me up. The AC unit served as a nice white noise background that would let me sleep through the night.

What about eating?

Our RV came equipped with a propane four-burner stove and also a microwave. The refrigerator was a little bit larger than a mini-fridge but was able to fit plenty of milk, juice, bottled water, Gatorade, and other snacks for the boys.

Every time that we would visit a new town, we liked to find the local eatery, so we actually never used the stovetop.

One time one of the boys accidentally turned the knob to the stove, and the RV reeked of propane. I read another review of another family that stayed in the RV and tried cooking, and they said it was like cooking in an oven. I could definitely see that being in such cramped quarters.

The bathroom. I think everybody always wants to know, okay, how big is the bathroom? Great question. I’m six foot, 210 pounds, and I could barely squeeze into the bathroom. I never took a shower in the RV, but my wife and boys did. Each campground that we stayed at had showering facilities, so that’s typically where I would take my showers.

9. What About Your Doo-Doo?

Oh, yes. Where does the doo-doo go? When we picked an RV, the guy at the rental place gave me a very brief overview of how to empty the pooper.

I thought I understood, but I do remember asking him the question, “Do you think I really have to empty it if we’re only going to be there for two weeks and we only use it when we have to?” That basically meant that if I could avoid emptying the pooper, I was definitely going to try.

The RV has a gauge that shows you different levels, and different tank levels. After the fourth day, I realized that eventually, it would have to happen. I was going to have to empty the pooper.

Luckily, we met a nice couple at the campground in Albuquerque, New Mexico, and the husband showed me how to do it. The next morning I had my first test, and it was a success.

Fortunately, I didn’t get sprayed or dripped on, thank goodness. Emptying the sewer is definitely one of the less glamorous aspects of using an RV, but it’s definitely not that difficult. I’m not sure how I pulled this off, but for the entire two-week rental, I never actually used the RV bathroom for the number two purpose.

It might be a bit too TMI, but I felt much more comfortable with using the campground facility versus the RV. Our boys, of course, had no shame or issues taking care of business inside the RV.

10. What Will You Miss the Most?

Going on a two-week RV trip, you tend to wonder the things that you would miss while you’re gone. Here are the 10 things that I missed the most.

- Two-Ply Toilet Paper. Do I really need to explain myself on this one?

- Loofah. At first, I felt like I could just carry the loofah to the campground showers and then carry it back, but then it was just another thing to carry on top of a change of clothes, toiletry bag, shampoo, soap, et cetera, so I stopped. The loofah was definitely something that I missed when I got back to take my first shower after being in the RV for two weeks.

- Decent Wi-Fi. We got spoiled at the first campground in that we were able to stream Netflix on our boys’ iPads, and we had fast enough internet for our laptop. As we got further on our trip, every campground offered Wi-Fi, but the speeds were questionable. I felt like it was 1996 again – worse than dial-up.

- Kids’ Bedrooms. I love my boys, don’t get me wrong. But having a little separation is nice. We typically put our boys down around 8:30 p.m., which gives mommy and daddy plenty of mommy and daddy time.

- When you’re in an RV, there are no kids’ bedrooms. You’re literally 15 feet from each other. Our boys like to wrestle, play and giggle, which often kept us up late at night. This video shows you exactly what that’s all about.

- Cross Fit. I don’t like to run, but I knew I needed to do some type of workout while I was gone, especially with the amount of food I was consuming. I missed my cross fit gym and throwing my Olympic weights around.

- Barbell Pull-up Bar. I love doing deadlifts and power cleans, and I missed the set I had at home. Every campground had a decent playground, but only one of them had one where I could have done pull-ups. A nice pull-up, pushup, and running workout would have been great.

- Small Group. At our church, we have a monthly Bible study, and I love the couples that are in our Bible study. We have great discussions and share our struggles and triumphs in trying to be a better Christian. Being apart from them for two weeks was definitely something that I missed.

- A Juicer. I love my juicer. After watching the documentary Fat, Sick, and Nearly Dead, I have been using it at least once, if not twice a day. I tried to tell my wife that I was going to bring it with me on the RV trip, and she just laughed.

- I remember her saying something like where the heck are you going to put that thing? Without garbage disposal in the RV, bringing the juicer definitely would have been a pain, so I didn’t bring it, but I definitely missed it.

- A Toaster. We could have brought a toaster, and it would have been fine. One of my favorite easy snacks is peanut butter and jelly, but I like mine toasted. Not having a toaster took away from my favorite treat.

Renting an RV – Trip of a Lifetime

On Day 11g, I remember that both my wife and I were a bit homesick, and we missed our king-size bed and down comforter. Despite that, we can both say that we and our kids had a blast. This trip was about making memories, and the hundreds of pictures that my wife took are a testimony of how many memories we created.

I asked her if she was ready to go on another RV trip, and for now, she needs a 365 break to think about it. I’m not sure if we’ll go on an RV trip next summer, and I can confidently say that we will go again.

Have you ever rented an RV? What was your experience renting an RV?

Thanks for the thorough review of costs and the experience. It helped me to confirm that RV-ing a vacation is not something that I want to do.

Thanks for article, very informative. Looking into the same thing!

Wow, Jeff, thank you for this post! We have a 25′ Cruise America reserved for a two-week trip from Chicago to the Grand Canyon in just a couple weeks, so it was great to compare with your experience. (Dog, no kids.) We’re able to take advantage of CA’s off-season rates, including .17/mile. But I was just looking at nationwide average gas prices and realized how much we can expect to spend there. Ouch, indeed. I’d been ignorantly thinking we’d get around 15mpg, but your 8.66 was a needed dose of reality. Also appreciate all your other tips and advice on KOAs, emptying the black tank, showers, side-trips, etc. – Dave

I enjoyed this journey. It did bring realistic cost to mind.

It is not cheap to do this.

My wife and I want to get a RV to travel around over the next 10 years. Across the US , Alaska and through Canada. I just don’t know it I want to spend the $$ or not.

Retirement decisions are so tough.????

Thank you for sharing

First I want to say, “Great article!” My husband and I are planning for a 14-day trip to Utah’s Mighty 5 +Grand Canyon with our 3 kids; 3, 8 & 10. This article was a perfect motivator! I’ve looked a lot into RV rental and decided to go with the 25′ RV from Cruise America (mostly because of the lower price tag compared with other RV rentals). One question – where/how do you place a carseat in the RV?

Thanks again for the tips, suggestions and experiences in this article!

Great read. I have owned a 36′ motorhome with 3 slides, that my husband always drove. We also always towed a car on a tow dolly. I always wanted a class C rv so I could drive it too. Not sure if I would also want to tow a car behind though.

Thanks for sharing.Very informative.

Thanks, that was really helpful. We are thinking of taking an RV from Michigan to the West Coast in a few years and this will help us budget money.

Hi Jeff,

Thank you so much for taking the time to write this blog! It has answered so many of my questions. I’m thinking of taking my two girls from Connecticut to California (where my family lives) this coming summer. The only company that I could find online that does one way trips is the same company that you used so this was perfect for me to get an idea of what the cost will be. I’m sure I’ll pay a premium for one way and I’m taking a month to do the trip but your mile count and info on gas, KOA costs etc. are invaluable!!! Thank you again! I’m excited about planning our trip and after reading this, I feel like it’s actually doable! Now I can use your info as a guideline to start researching and planning my itinerary. Happy New Year!

–Kim

Hi I read your story sounds great I trying to talk my husband into doing the same trip we have a camper but it stays in the campground all year it’s not road worthy anymore I live in NY and I want to travel on a trip of a lifetime thank you for your it was great to read Chris

I am a mobile RV tech in Sedona AZ and an avid RVer. A couple of tips:

Many of the tech skills that you need to operate any RV are outlined on line either in forums or YouTube. However, Jeff is correct in saying that it can be hard to find good WiFi in most RV campgrounds, so you may have to run to the local fastfood places – McDonald’s, Burger Kings, Walmarts, or internet cafes to view the videos or do the research when you have a problem operating the RV.

If you are going to visit 4 or more National Parks, purchase the annual pass for $80. You will come out way ahead as this pass gets you into all national parks and monuments for 1 year from date of purchase. We just returned from Yellowstone which is $35 per vehicle per day.

Good tips, thanks Brett!

Jeff, thanks for writing out such a thorough description of your experience with RVing. It can get complicated!

If you were to do it again, would you rent from a private RV owner like with AirBnB? I ask because I help out with the private RV owner community at www.outdoorsy .com, which generally offers less expensive RVs with more amenities. Some owners even include cleaning and kitchen supplies.

Thanks for the interesting read about renting RVs! It’s interesting to learn that there are a lot of available places to stay with an RV such as campgrounds with different amenities to boot. It seems nice to have either the camper or the RV since the only difference is that there is less interrupted driving time in RVs. I’ll try renting either an RV or a camper this coming summer for our trip. Hopefully, it’ll end up being a lot of fun for my kids!

Jeremy, I’m sure your kids will love it, it’s like they get to pick their own fort to camp in. Let us know how it goes!

Thanks for the great RV info. I’d like to do a (one way!) trip this coming Summer. Will take my best sales skills to convince the Missus…

Love the Cousin Eddie impersonation!

NJB

I found your 10 tips when I was researching renting an RV. I enjoyed the straight forward description, plus the humor that you used. We will be thinking real hard about renting an RV. I ‘m glad your family had a great trip.

You gave your family something that they will remember for a life time.

Dave.

We enjoyed your article. We felt like we were on the trip with you.

There are a lot of private owners of RV’s who rent them out on RV rental websites and the costs can be quite a bit lower. Happy Road Trips!

Great writeup. Extremely hilarious and brutally honest. Did not realize it was a quarter as expensive as it really is!!!! I may wait til we retire. Your wife has the most amazing legs BTW!

D

Thank you for being so detailed! We are a family of 7 so I could totally envision what you were describing. Thank you for including the gas cost. This gave me a lot of information I couldn’t find elsewhere as I am planning our summer getaway! Thank you for sharing!

Thanks for sharing the details of your trip! I found your link by searching for RV rentals and it provided a very realistic idea of the costs. When I was a child, my good friend brought me along on an RV trip from San Diego to the Morrow Bay Area. Also, my parents used to take us on a cross country road trip every summer in our car (California to the east coast). It was really difficult traveling so far in a car, but we stayed in hotels or with friends every night. I would love to combine the two ideas and do a cross country trip with my kids in an RV. Thanks again for the post!

Hi Jeff. I enjoyed your article. Im now retired, never RVed but Im getting a little bored (it’s only been one month and Im looking for things to do). Ive been playing around with the idea of hitching my SUV to a 17 foot Casita and just going around the country–actually thought I should rent first, but considering buying. Anywayyy, I would be traveling solo as my family are all grown up and have better things to do and I was wondering if you met any solo RVers on your travels and if they were happy (or not) with traveling alone. Thanks, Ken.

@Ken I don’t recall coming across too many solo travelers. Then again, we were doing our best to keep our 3 boys under wraps so we were a bit preoccupied. 🙂

I am a retired female. I have been traveling solo for nearly 3 years. There are plenty of us out there. Most times, if I am feeling lonely or bored, I just strike up a conversation with someone. I dress to blend in, therefore no one knows I am alone.

I am a retired female. I have been traveling solo for nearly 3 years. There are plenty of us out there. Most times, if I am feeling lonely or bored, I just strike up a conversation with someone. I dress to blend in, therefore no one knows I am alone.

Hey Jeff,

It’s a great piece of sharing your experience, which answers a lot of my concerns. I am grateful for your effort. I am also planning on a 30-day RV road trip. Can you tell me which is a cheaper way to do it, buy-use-sell or rental? Any information is appreciated, thanks!

@Pengyun It’s hard to say because there are so many variables. I would think renting from a private owner would be the most affordable way to go.

@Penqyin,

I have 6 RV’s, Class A, B, C’s for rent in Grand Rapids MI that you can take anywhere in the US. Check out my site at www. DavesRVs .com

Thanks,

Dave

Hey Jeff we just went on our first RV trip and it was awesome. I have to say it’s been my families favorite vacation in the last 10 years. We got a really good deal from a private owner on the rvshare website. I found the price at the end of the day to be a little cheaper renting from a private owner. Here’s the website we rented through in case anyone else wants to check it out: https://www.rvshare.com

Great Article, really reflects what renting an RV is like. I especially enjoyed the part about missing the juicer. My thoughts exactly XD. Life is just not the same without my avocado flaxseed smoothie in the morning! We used these guys www.campanda.com because they have locations everywhere even in calgary which is where we wanted to pick up the coach!

Hi Jeff,

That was some great information! We are traveling from Australia to LA in December and plan to RV it around for about 12-13 days. We have never done it before so were wondering about the cost of the generator? Since we will be traveling in winter, will we need to run it all night for warmth! What if we park at a campground? Does the generator basically just keep the power on? Sorry, not sure how it all works. It will be hubby and I and our two kiddies 8 and 6.

Thanks kindly.

@ Bonnie From my understanding having the power hookups is huge so you don’t have to run on the generator. All the campgrounds we stayed at offered power so it was never an issue and we ran our air conditioner all night.

If I recall correctly, we would have been able to run on the generator for at least one night (maybe two?) before having to recharge.

Most RVs can run heat without the use of the generator. Ours uses the 12V battery to run the heat, the heat consumes propane, but the propane lasts for many nights on one fill-up (weeks of nightly use in moderate climates). If you were camping where there are no hookups, you will need to start the generator for about an hour once every day or two, to recharge the 12V battery.

Hope this helps,

Josh

Great article. My family and I (wife and 4 teenagers) took a 10 day RV road trip from SC out to Colorado and back a few years ago. Had an awesome, family bonding, memory making time. My best advice is to take Duct Tape and buy the Insurance offered where you get the RV. Be aware that there is no depth perception on the older RV backup cameras, therefore you are likely to back into a mountain while doing a 9 point turnaround on a narrow canyon road – like I did in Sedona. Had to duct tape the whole back side of the RV all the way home from Arizona to SC.

Hey, if Duct Tape is good enough for NASCAR, it is good enough for me.

I have a question I am hoping someone here can give me an honest and unbiased answer to. How safe is it to travel in an RV and stay at KOAs?

I am a single 46 year old woman with 2 teenage daughters. I am thinking about taking a RV along the Ca coast from San Francisco to Seattle next summer. I had a friend tell me I was crazy for wanting to take my daughters on the open road alone. Am I?

@Lana I always felt safe in all of the KOA’s we stayed at. Even more so at the locations that were closer to tourist areas as those KOA’s were much more crowded with a ton of family activities.

Travel is such fun, and we’ve done lots. A few reminders: comfort is important when traveling, whether it’s a tent or r.v. Bring things that you know you ‘need’..the toaster is one. The chef’s knife you love. The cast iron fry pan you make steak on. good rain gear, good hiking gear and clothes for both hot and cold climes. Bring the bed clothes you love..that neck pillow, the comforter..yes! We ended up buying a cheap camping gazebo on one trip to cook under. Plan for wind and rain. As for pets, you can’t leave pets alone in most campgrounds. Sometimes other campers are rude and noisy..even irresponsible. It happens. and remember, warn the kids to be not afraid, but aware, of snakes. Share the wilderness, right? And make new friends.

Great article. But for me have to pack up suv travel 2hours leave my car would be hard. Rather be able to pack from home. Sounds really expensive yet all vacations are. I as going to buy one but after joining an rv site and asking a lot of questions I’ve decided not to. It’s always been my dream but even renting cost more than my Disney trip and we went to all the Orlando parks even swam with the Dolphins. I guess if I was rich I could make this dream come true but for the average joe can’t afford either.

Great article! Another good resource for finding an RV rental is https://RVshare.com it’s like the Airbnb for RVs. You can rent RVs directly from private owners.

Thank you so much for this thorough account of your RV trip!! It was very helpful. My hubs and I are planning on taking our 4 young kids out West to visit family this summer. It was a blessing to read through your experiences and this has helped me very much in learning more about the whole process. God bless you and your sweet family.

Awesome post. We are about to venture into the rv world. We are looking at buying a used one.@15,000 or renting. Are kids and grands live on the east coast and we on west. Would like to travel many states while we are in our retirement. Being retired truck drivers we got to see the world through the windshield now I want to enjoy it.

Really good post Jeff.

I’m a Chinese and living in Missouri currently. I saw some American movies about RV trip like we’re the millers and saw a lot of RVs when I m driving in interstates. An RV trip is one of my dreams since driving and sleeping are my favorite things. Your post reminds me there are also some annoying things of an RV trip. But I can find that, you enjoy your trip pretty much. Hopefully I can have a wonderful RV trip like yours with my family or friends one day

By the way, don’t you think an RV towing an SUV is the best option?

@HD Definitely having a car behind the RV would be very convenient! 🙂

Thoroughly enjoyed this account. We are partly retired, and looking to buy an rv. I grew up every summer visiting west, family in california and utah. About 12 of those years were in 2 camper vans, ford econoline, and later a vw. Slept 6! It had the canvas popup on top, where my 6 ft brother slept. Another canvas sling below him, and my parents below that! The canvas sling bed over the front seats held me and my 4 yr old brother. The fridge held an iceblock. Toilet was a pullout box with lid and toilet seat, with strong plastic bag inside. We went throughout Mexico, remote fishing villages on Baja, through Canada, etc. We got to every u.s. state at least twice before I was 12, except alaska, hawaii, and florida. Best gift my dad ever gave us. So, we plan to buy a Roadtrek or Pleasure Way Class B 18 ft van. Funny, we just did a guided 9 day tour of Grand Canyon, Zion, Bryce, Sedona, Vegas, with friends. About $2000. each. Had a blast. Thank you again for your great account!

Also, my dad loved KOA Campgrounds, even back in the 60’s. It was our job to read the maps and campground book(big like a phone book), and find a place to stop each night. I remember one morning waking up close to a cliff edge, over a rushing river.we had pulled over late, off a country road!

Sorry… the tour was via hotels with a tour company.not camping. Beautiful area to visit!

Incredibly helpful! I am looking to take an RV trip as soon as I receive my diploma. Thank you for the detailed post.

So helpful!! We are renting an RV to go to Colorado to visit our son for a week. The reason we decided to rent the RV is because we are taking along our 3 dogs! No hotels will accommodate us and this way they can be with us at all times. I did a cost comparison to renting the RV vs. hotels. Your blog helped me figure out some of the costs, (ie: gas) Also gave me some insight on the space. In preparing for our trip I have referred back to this several times! Thanks so much for sharing!

Great post. Being grandparents, and hopefully retired in 5 years, we are anticipating trips with the Gkids. Just looked at RVs this past weekend and I wondered “what if we just rented for the occasional trip instead of buying one”. Why pay all the storage and maintenance fees if we only do one a year or so?

Anyway, your trip story opened up more discussion and provided a better trip cost analysis and planning.

Thank you so much for your post, we are looking to rent an RV during the Christmas holiday to drive from NJ to FL and this is so informative. Flights are so expensive during the holidays and it seems like it would be the same or even cheaper to rent an RV than Fly for a family of 5. I do have 2 questions one is I see you mentioned you traveled with dogs how did you do with them when you stationed somewhere? was it ok / safe to leave them in the RV for a few hrs if you were sightseeing etc? I assume you would leave windows open etc correct? Also we would be headed to Orlando would we have to be stationed daily at a campground or can we park RV at a residential location if we are visiting family etc? Any further information you can share would be great. Debating on flying/hotel expenses or renting an RV to travel instead in. Also do you know anything about the ones that pull / tow your own car so we can move in our car while in FL vs the RV?

Very informative post! Thanks!

I really enjoyed your story it is a dream of mines to rent one for 14 days and travel from Jonesboro Ga to Las Vegas staying different campsite it would really help if you could email me some of your info on where to rent cause some of the place I have been checking is really to much but I want this trip so back it called the family journey so really it to site see please help me thank u so very much.

If all the headaches and costs provide a superior experience over the ease of motels — why not do away with the majority of the costs and use a tent?

Our family can NOT stop laughing! Your post is not only extremely informative, but also an absolute loving challenge! We are so ready to do this in the summer! Thanks for answering all of our questions.

Hi Jeff…I have done 3 similar trips..2 with class C and one with Class A from El Monte RV. Each had slide outs. Traveled with adult son, granddaughter and my spouse….and 4 dogs. Your travels mimicked mine. I would not rent without the slides. It made for much better room with all of us. The adventures, the conflict resolutions, the sharing…you cannot put a price on it and well worth not staying in a hotel or a singular place for a week. It was always fun spending a day or 2 at a site to get to know people a little. I was astounded at how helpful other RVers were along the way with sharing hints and time. El Monte reduced our costs with some discoveries..poor tires, out of alignment issues on various rigs.

Good article. We are retired military and travel in our RV about 9 months a year. We love the lifestyle; reminds us of PCSing adventures.

Regarding other vacation options…have you ever tried the Armed Forces Vacation Club? Before we got into RVing that was our go-to travel resource. $299 for week-long condo rentals all over the world.

Loved the article ! I have been wanting to take a trip in a RV, but after reading this, IDK….The cost is higher than I expected, although I really want to do it some day, I don’t know when that will be. Usually this time of year we (my husband and I), as our children are grown, are lying on a beach in the Riviera Maya. That is much less expensive and we do stay at gated resorts that are four to five star.

In 2013 our home of thirty+ years burnt to the ground and we are still not home yet. I don’t know what is in the cards for us, but one day, yes, I would love to do this.

I enjoyed reading your article, thank you so much for posting. Your family is beautiful !

Great article. We’re taking an RV trip to Red Rock State Park, AZ from San Antonio, TX area for spring break 2015. We’ll have it for 8 nights. I figured out the cost except for the gas. This really helped. Lucky for me gas prices have gone down about $1 a gallon since your trip.

And speaking of cost, my trip will cost about $3500 and I’m sure we could do it for half that if we stayed at hotels or cabins at some of the state parks. We travel a lot and even renting a house with nice amenities, as someone else mentioned, can be much cheaper than an RV. But, the experience will be worth it I’m sure. I’m definitely looking forward to no potty stops, less fighting and no passing electronics and food to the back seat.

Some questions I do still have are, do I need my own cleaning supplies like cleaner, broom, dust buster, mop? My kids will be 8 and 5 when we travel. The crumbs and dirt on the floor will drive me crazy! Also, do you leave your car at the RV place? Is there an extra charge for car storage?

@Lana Yes, you will need to bring your cleaning supplies. I think they provided a broom and dust pan, but that as it. We had to sweep it out minimum once per day, usually twice.

We did leave our car at the RV place and there was not an additional charge for this.

And yes, you will save a ton on gas! #jealous

I was laughing to my wife the other day while at the gas station, “Do you know how much we would have saved in gas money if we did the RV trip this year?”

🙂

We’re taking a trip next summer and definitely balanced the cost of RV vs. Hotel. The big difference for us is we live in Souther Cal and we want to travel around National Parks in Colorado, Wyoming, and the Dakotas, so we’re foregoing the 2,000-mile round trip and flying cheap to Denver to kick-start the trip. We would need to rent a car anyway, so this evens out the cost difference between doing RV and cheap hotels.

We also are traveling 6 together – my wife and I, two kids (4 and 6) and my parents – so having the large RV with separate “bedroom” becomes even more reasonable, considering we’d have to get two rooms or pay more for an extra-room suite. All in all, our flight and RV rental for six people, 10 nights, comes to $3,400. Add in all the costs mentioned in the article (we’ll have about 1,700 miles on our trip, so less gas and a lower mileage fee; we also plan to eat cheap cooking for ourselves, since we’re used to cooking outdoors anyway) and it’s likely to come close to $5,000. Considering we can hop on a cruise ship locally and have an easy yet fun trip for <$500 person, the RV trip will certainly cost more… but we're sure it will be worth it!

We would like to get an RV one day and I had thought about renting one in the meantime, at least once. From your post, it would be very expensive for us. One thing we like to do, is to rent a house, like we did in Florida. We had kayaks and bikes and the owner waived the $100-$150 (sorry I can’t remember the exact figure) cleaning fee because we cleaned it ourselves. It was a beautiful home, with tile flooring and its own private pool. I think the cost for the whole week was $600 or $700 something. Also, when we stay in motels, we usually pay less than $100 a night. We also like bed and breakfasts when it’s just my husband and me. Just thought I would pass along these thoughts.

I just don’t see how this is cheaper than staying at a hotel. I guess if you are getting two rooms perhaps.

It may not be cheaper. But it’s convenient to wake up in the RV right at the national park or other ‘away from city’ environment. I was going to buy an RV, then decided to rent…..but after reading this, I have to think about it all over again! My wife and I enjoy sitting out in the woods w/a campfire. Price is not a concern, and they all seem priced comparable to me w/the exception of owning which would be more.

This is really interesting! I had been thinking about this – or rather, my husband had been bugging me about it – but was curious about the costs! Not going to lie, I expected the fuel bill, but no the rental costs. It seems like there might be better vacation value elsewhere.

Campsites do not have to be quite that expensive. If you can do without some of the amenities (wi-fi, pools) you can typically stay at state parks for $15 to $35 per night. The higher end usually gets you waterfront sites.

The lack of potty breaks and easy access to snacks seems attractive, but I can’t imagine how hotels would be “obviously….much more expensive.”

If you used a basic hotel site such as hotwire/priceline I’m certain you could find quality hotels in most any locale for under $150/night, probably less than $100 in many places.

Also consider the gas consumption in your SUV would be much, much lower.

I enjoy camping with my family and realize the experience you’d get at a campground vs. hotel are much different, but you also have to factor in the cost that you paid to stay in the RV most nights. IMO this trip would have been much cheaper via hotel.

It most likely would have been not nearly as much fun, but I can’t imagine how using your personal vehicle and mid-priced hotels could be overall more expensive.

Great review! We have been thinking more and more about possible renting or even buying an RV or a pop-up camper. We went on a 2 week road trip around the same time as your family did and we took our Wrangler everywhere. It was cramped!

The RV trip is definitely on our list of things to do, but I’ve always worried a bit about the cost, the hassle of emptying the pooper, and driving that huge thing around everywhere. I think you’ve answered a lot of the questions I might have had – and you gotta love the cousin Eddie tribute photo!

Thanks for sharing such a thorough review of your RV trip. Our family has always wondered what costs were associated with going RVing. I think your article covered the topic well. I definitely think we will try it one day but probably not quite yet since our kids are only 2 and 4, I think it would be more trouble than its worth.

Great article! My wife and I have been wanting to take a vacation like this forever. We want to rent an RV for an Alaskan vacation. Article helped me understand some of the costs and so forth. Thank you!

Great post friends.

Jeff-

Very cool post.

I really enjoyed stalking you guys online during your trip. It was fun.

It’s cool to read about the ups and downs of going on a trip like this.

This is something I would like to do someday.

-Derek