If you have been wondering what it means to invest in digital real estate, you’ll have to start thinking in terms of our virtual world. In the rapidly evolving world of cyberspace, digital real estate is akin to a virtual parcel of land.

Investing in digital real estate allows you to own a piece of cyberspace — a digital asset — that can be made available for sale, and to use that piece of real estate in any number of ways.

However, the types of digital real estate that are out there are a lot broader than you might think.

For example, the website you’re reading right now is a piece of digital real estate that I have grown and nurtured for more than a decade of my life!

The ways you can make money with digital real estate are also nearly limitless, as I’ll explain in more detail below. If you’re ready to find new ways to invest virtually for the future, read on to learn how digital real estate investing works and how to get started.

Digital Real Estate vs. Online Real Estate Investing

Table of Contents

- Digital Real Estate vs. Online Real Estate Investing

- Examples of Digital Real Estate

- #1: Authority Blog: GoodFinancialCents.com

- #2: YouTube Channel: Wealth Hacker

- #3: Podcast: The Good Financial Cents Show

- #4: Online Store: Bumblebee Linens

- #5: Online Course: Passive $1K Formula

- #6: Social Media Account: Kendall Jenner’s Instagram

- How to Invest in Digital Real Estate

- How Much Money Do You Need to Invest in Digital Real Estate?

- How Do You Make Money from Digital Real Estate?

- Pros and Cons of Investing in Digital Real Estate

- The Bottom Line on Digital Real Estate Investing

Before we dive into all the different ways you can invest in digital real estate, I want to take a moment to explain how digital real estate is different from other types of hands-off real estate investing. For example, I frequently talk about real estate crowdfunding platforms, as well as investing in Real Estate Investment Trusts (REITs).

You could invest by purchasing fractional shares of a stock or buying an index fund that includes a basket of stocks that meet specific criteria.

More importantly, platforms like Fundrise actually let you invest in physical property instead of digital property. In fact, Fundrise investments typically include planned communities, high-rise apartment buildings, and commercial real estate.

| I’ve been investing with Fundrise since 2018. Disclosure: when you sign up with my link, I earn a commission. All opinions are my own. |

Examples of Digital Real Estate

With all that being said, pretty much any type of digital asset you can buy or sell can be counted as digital real estate. In fact, the types of digital real estate you can find today extend far beyond simple websites like the one you’re visiting right now.

Some of the most common examples of digital real estate include:

- Affiliate websites that earn passive income.

- Assets and land sold in the metaverse.

- Authority blogs that focus on a specific niche.

- eCommerce stores that sell physical products.

- Digital products like courses and printables.

- Domain names that are bought and sold on websites like Flippa.

- Email lists that are built and sold to others.

- Membership groups that require a monthly or annual fee.

- Mobile apps that are built for a specific purpose.

- YouTube channels that are ultimately monetized.

- Social media channels that are grown and monetized

The examples below highlight some of the types of digital real estate people can use to earn both active and passive income.

#1: Authority Blog: GoodFinancialCents.com

Welcome to one of my digital real estate investments, my website GoodFinancialCents.com. As a financial advisor, I use my authority blog to teach people about personal finance and the tools they can use to build long-term wealth.

While it wasn’t always the case, this piece of digital real estate is fully monetized and highly profitable. Not only do I earn passive income from GoodFinancialCents.com, but I could sell this virtual parcel of land for a profit if I wanted to.

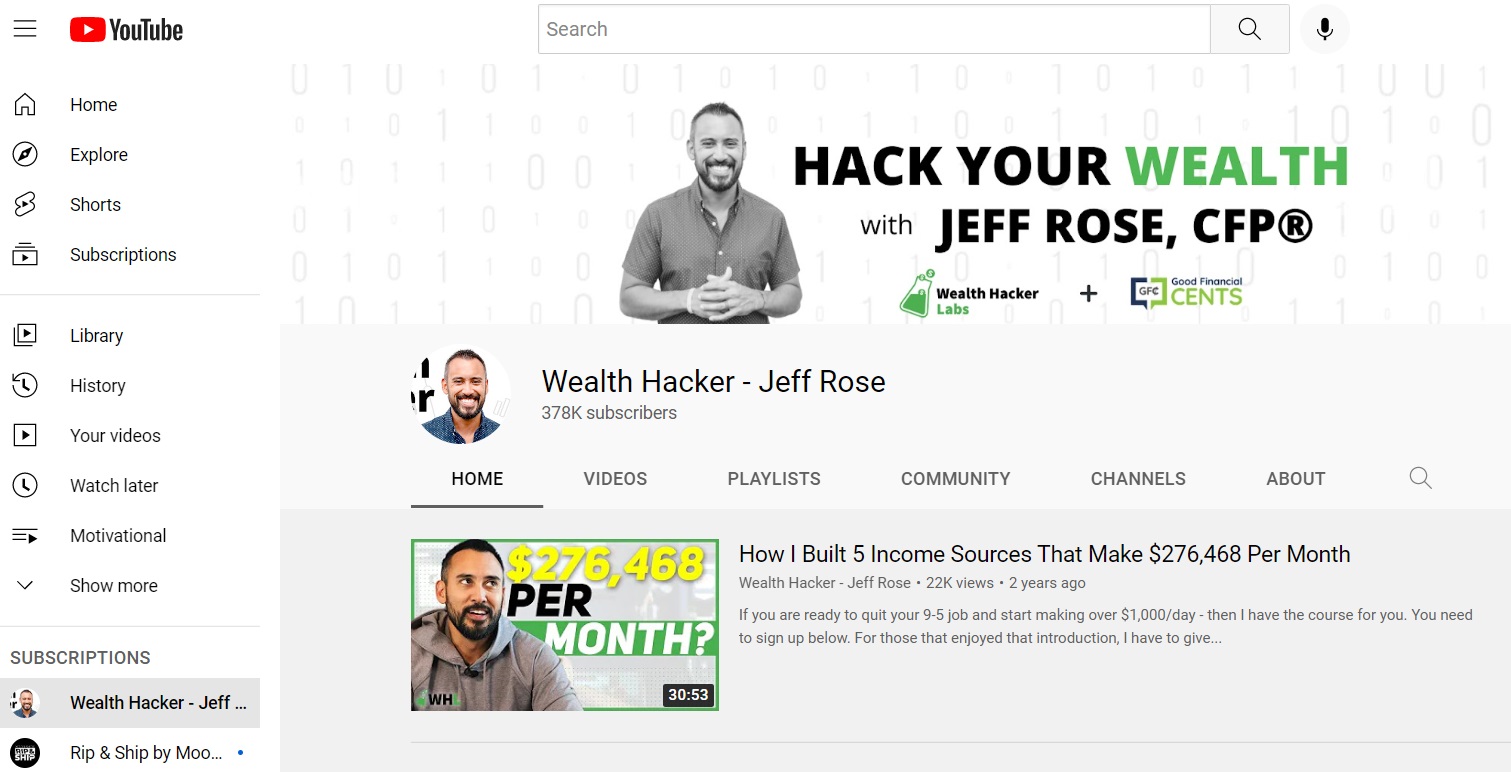

#2: YouTube Channel: Wealth Hacker

My YouTube channel is another piece of digital real estate I own and leverage to build wealth. Wealth Hacker covers many of the same topics as my website, yet it makes sense to offer video in addition to written content.

Most of the videos on my YouTube channel focus on teaching others how to make more money, but I also talk about things like how to find a mentor, the best investment platforms, and money mistakes I have made in the past.

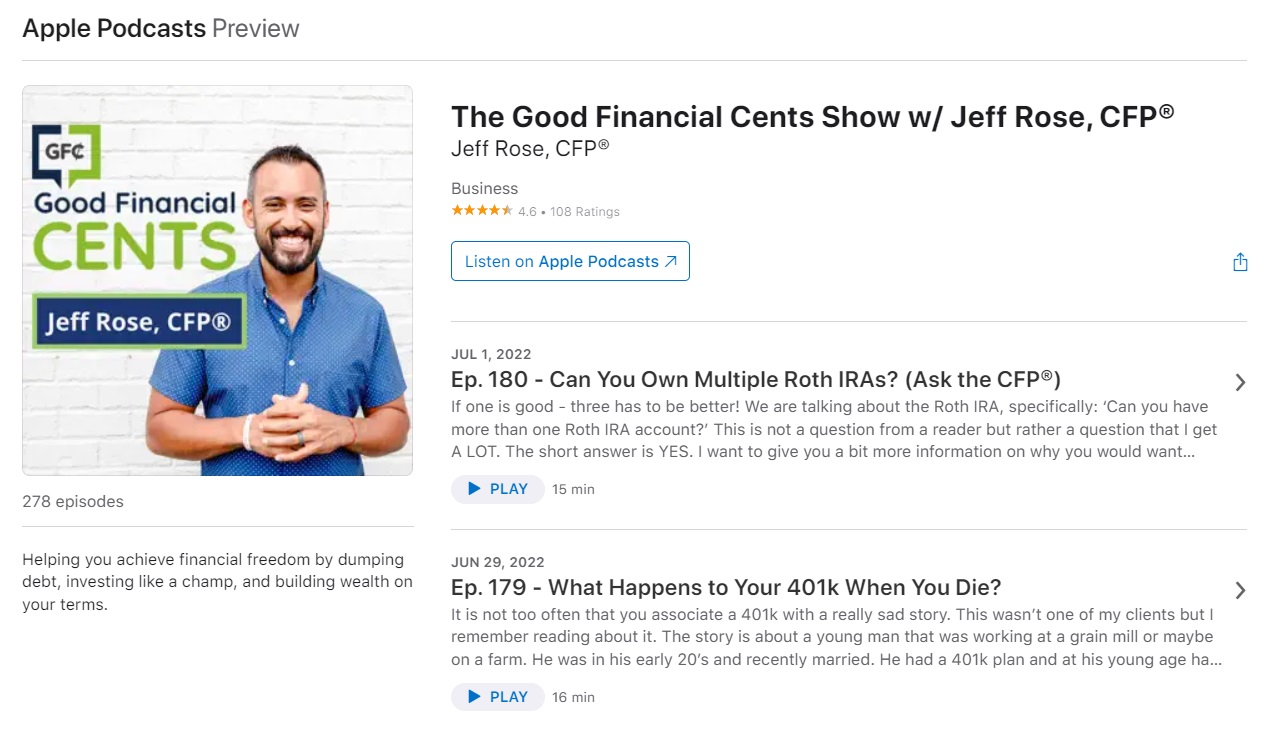

#3: Podcast: The Good Financial Cents Show

Another piece of digital real estate I own comes in the form of a podcast. I use this podcast to reach even more people who might be inclined to listen to recorded content while they exercise or commute to work.

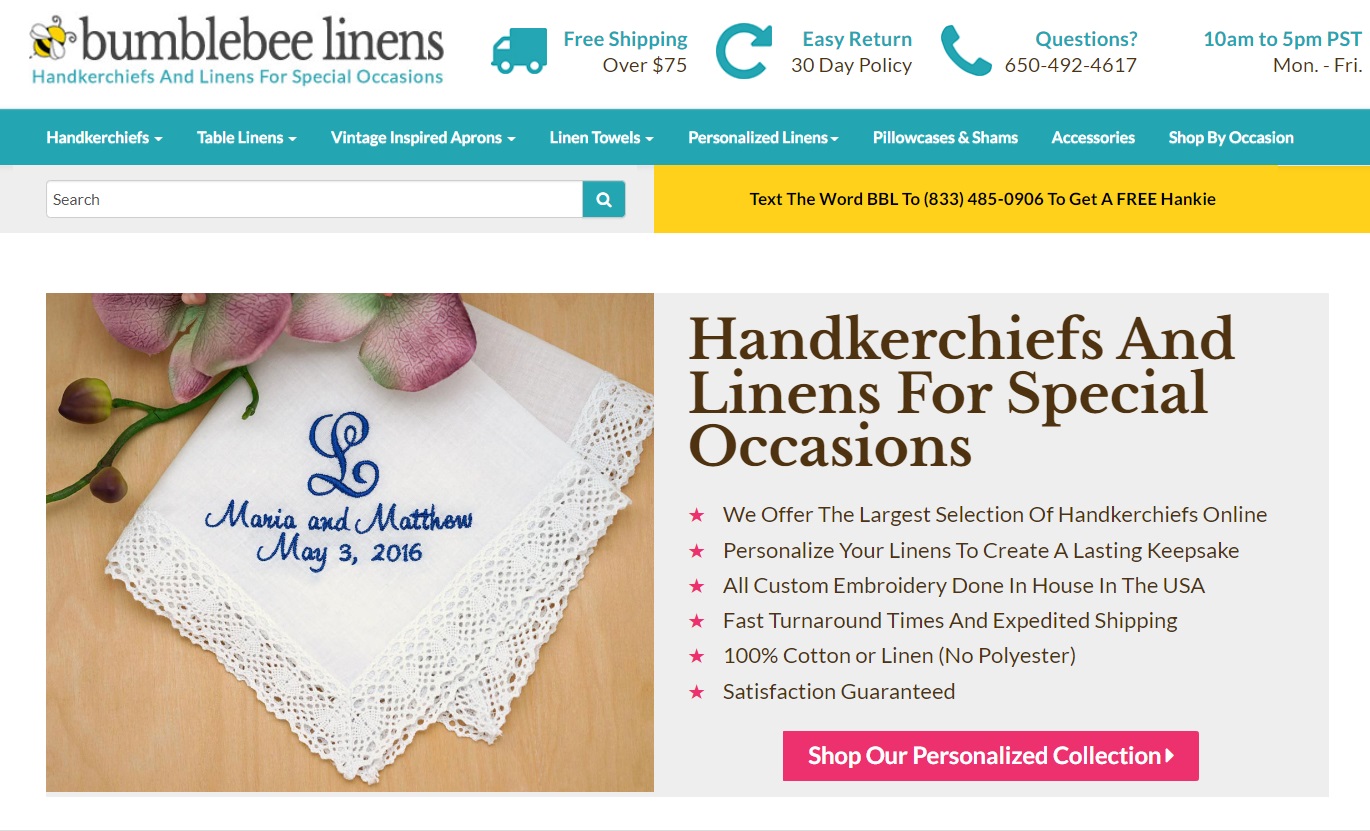

#4: Online Store: Bumblebee Linens

My friend Steve Chou, who runs the website MyWifeQuitHerJob.com owns this virtual store that sells personalized handkerchiefs. Not only does this piece of digital real estate earn passive income through sales of their product, but it could be sold to an outside investor for a massive profit.

Another example is an online store called Compete Every Day, which is run by a friend of mine Jake Thompson. This website was built from the ground up, and it makes money selling workout apparel, books, and more.

#5: Online Course: Passive $1K Formula

Online courses are another type of digital real estate people use to build passive income, and I have a few of my own. This specific course, called the Passive $1K Formula, helps people learn how to build passive income streams on an entirely remote basis.

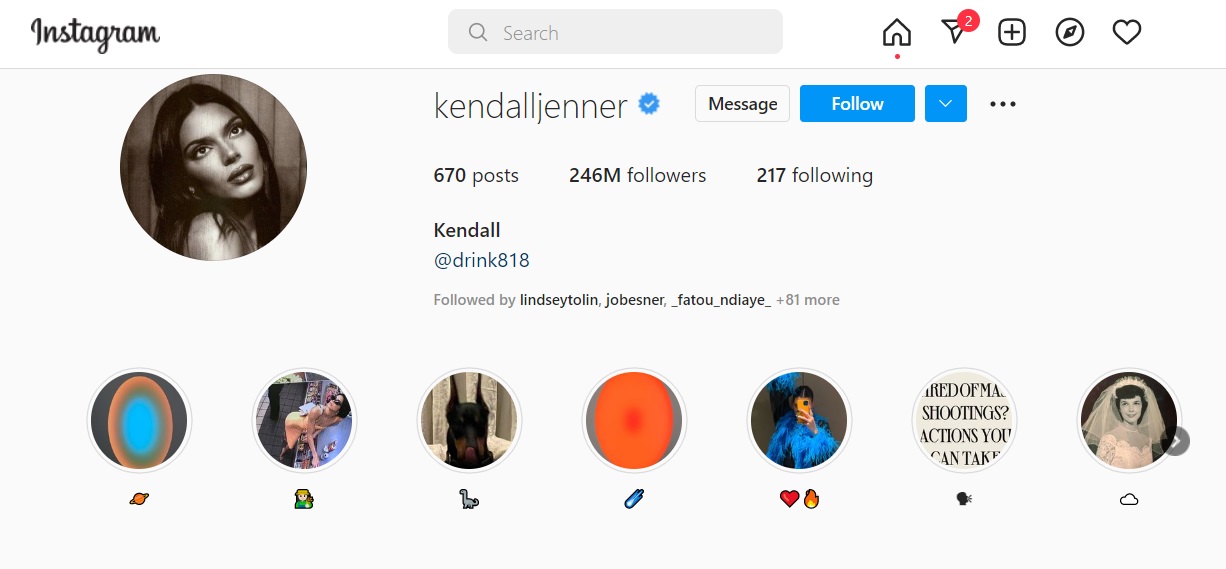

#6: Social Media Account: Kendall Jenner’s Instagram

Social media accounts that are grown and monetized can become a form of digital real estate you can use to build somewhat passive income. When you build up a ton of followers, brands will pay you money to share their products and services.

Kendall Jenner’s Instagram account with more than 246 million followers is a very extreme example, but you get my point. According to some reports, the model gets paid more than $600,000 for each sponsored post she shares on the social media platform.

Another example (of course!) is my Twitter account. I’m no Kendall Jenner, but I do have more than 30,000 followers and get paid to include social shares in various sponsorship deals.

Also check out 𝐓𝐡𝐞 𝐀𝐫𝐭 𝐨𝐟 𝐏𝐮𝐫𝐩𝐨𝐬𝐞 Twitter account, which reportedly makes six figures tweeting about art and various business and self-improvement projects. This Twitter account also has a link to a masterclass you can sign up for in their bio, so you can bet there’s some solid monetization going on through that course, too.

How to Invest in Digital Real Estate

If you are wondering how you get started investing in digital real estate, you should know there are a variety of ways to buy in. Some digital real estate investments require a different skill set than others, but nearly anyone can invest in digital real estate in some way, shape, or form.

Ready to invest in virtual real estate? Consider the strategies below.

#1: Build Your Own

First off, you can always begin building up your own piece of digital real estate that you can use to create passive income or sell for a profit later on. I’m talking about starting your own blog, building a YouTube channel, or even starting your own podcast. Any of these strategies can cost you a few hundred bucks or less to get started, yet there are truly no limits to the amount of income you can earn.

Just remember that building your own blog or digital platform takes a ton of time and patience. I didn’t earn much at all from my website during the first few years, but that started to change once I built up some momentum.

In many cases, you also have to offer something free in order to begin building up your mailing list and growing your brand. As an example, I still offer a Make $1K Blogging Free Course for anyone who wants to sign up.

While it took years for all my hard work to pay off, it definitely has! These days, I’m earning seven figures per year with my blog, my podcast, and my YouTube channel, all while working no more than 25 hours per week.

#2: Buy Digital Real Estate

Maybe you don’t want to spend time building up your own platform, or you like the idea of building on something that already exists. In that case, you can buy an array of digital assets from other people using various platforms.

For example, a website called Flippa makes it possible to buy or sell any number of online businesses. You can use Flippa to buy affiliate websites, authority blogs, eCommerce stores, SaaS businesses, mobile apps, and more.

Another website called Motion Invest has similar digital offerings. Just like with Flippa, you can buy digital real estate here and then sell your asset for a profit later on.

#3: Buy a Social Media Account

You can also buy social media accounts, although this type of digital real estate sale is currently in the midst of a transition. At the moment, you can use websites like FameSwap.com and SocialTradia.com to buy Instagram accounts and other social media accounts.

In the meantime, you can also buy various types of groups or memberships, including Facebook groups that are focused on a specific topic.

When you buy an existing social media account, you get to benefit from having that audience right away, and from not having to spend years trying to rack up followers on your own.

How you monetize from there is totally up to you, but you may be able to earn money through sponsorships, sponsored ads, affiliate marketing, and more.

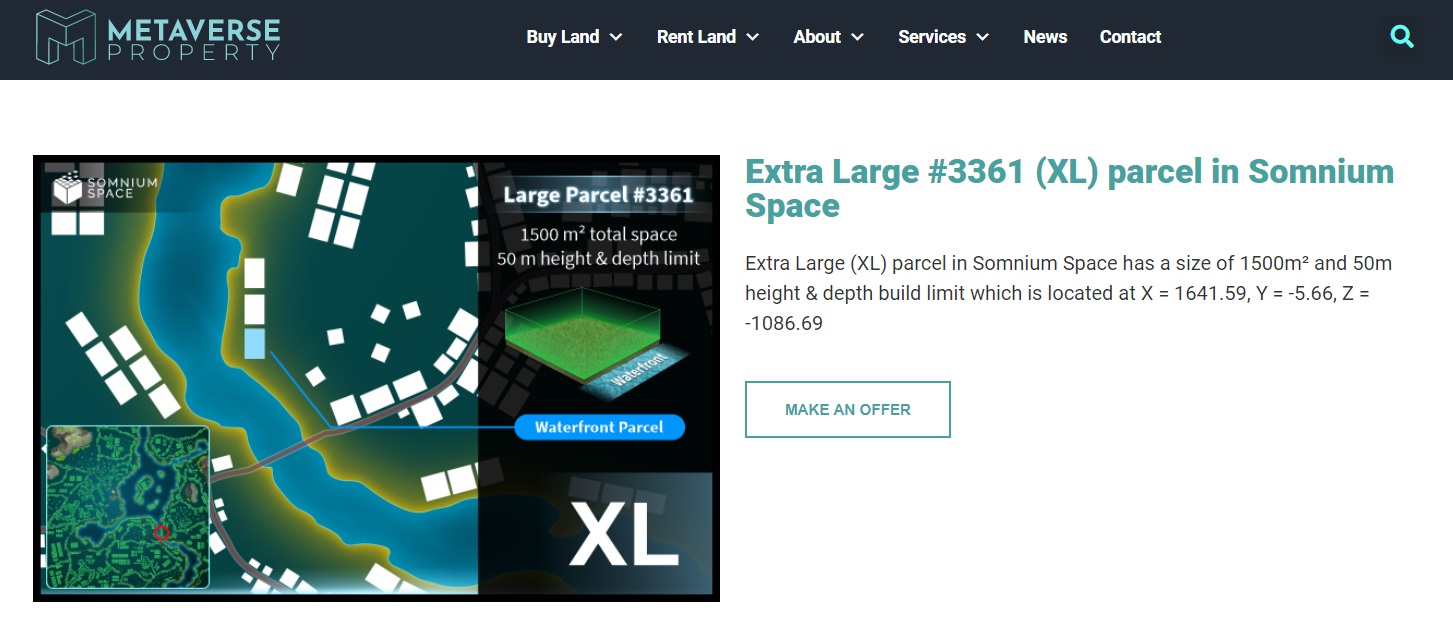

#4: Invest in the Metaverse

This final strategy is one that’s still in development, but it’s entirely possible to buy or rent virtual “land” or property in the metaverse. How do I know? Because there are platforms that let you do exactly that.

As an example, a website called Metaverse Property offers digital real estate of all kinds, which are actually just a form of non-fungible tokens (NFTs).

You can also use this website to buy property in Upland, which Metaverse Property explains as “the Earth’s metaverse where you buy, sell, and trade virtual properties mapped to the Real World.” Apparently, you can become a digital landowner or run a virtual business that has the potential to earn UPX coins, which are a type of cryptocurrency.

How Much Money Do You Need to Invest in Digital Real Estate?

In terms of investing in digital real estate through various platforms, you should know that the minimum requirements for entry vary quite a bit. However, there are plenty of ways to get started with small sums of money. For example, you can invest in physical real estate with Fundrise with a minimum account balance of just $10 and grow it from there.

How much cash you need to buy digital real estate depends on the type of virtual property you want to purchase. As an example, you can start your own blog for as little as a few hundred dollars, but buying an existing website that earns money could set you back a few thousand bucks or hundreds of thousands of dollars in cash.

Likewise, you can start your own social media account for free, but buying an account that has a ton of followers already will set you back a pretty penny.

If you don’t have a lot of cash to get started, you’ll be a lot better off trying to build your own parcel of digital real estate from the ground up. In this case, you can pay as little as $2 for a domain name through a website like GoDaddy, and then get started with a free WordPress theme. You’ll have to pay for hosting, but that can cost as little as $3 per month through a company like Bluehost or HostGator.

If you’re curious what else it takes to build your own website, check out the following resources:

How Do You Make Money from Digital Real Estate?

Monetizing your own digital real estate takes time and patience, and you’ll also need to research all the different ways you can make money online in the first place. Here are some strategies you can use to build passive and active income via the web, and through various means.

- Advertising: Most websites use some form of advertising to bring in revenue, such as display ads through Google AdSense. When you use ads on your website and a reader clicks on one, you earn money. When a ton of people click on your ads over the course of several days, weeks, or months, that’s when the real money starts rolling in.

- Affiliate marketing: You can also use affiliate marketing to earn money online. This type of marketing requires you to put links to various products on your website, and you get paid when someone clicks on a link to make a purchase.

- Membership site: You can also use your digital real estate to build up a membership site. This is a great way to generate passive income, and you’ll be surprised how much your profits add up when you get enough people to pay monthly fees to belong to your exclusive group.

- Product sales: You can also sell your own products online, which gives you ultimate control over your income and the potential to earn a lot more money. Online products can include anything from ebooks to online courses.

- Sponsored content: Once you build up your platform, you’ll begin getting offers from brands who want you to talk about their products. Sponsorships can easily pay hundreds of thousands of dollars at the higher end of the scale, but you may only earn a few hundred dollars for sponsored content at first.

Pros and Cons of Investing in Digital Real Estate

With the way everything is moving online these days, investing in digital real estate definitely seems like a smart idea. That said, there are some serious advantages and disadvantages to consider before you dive in.

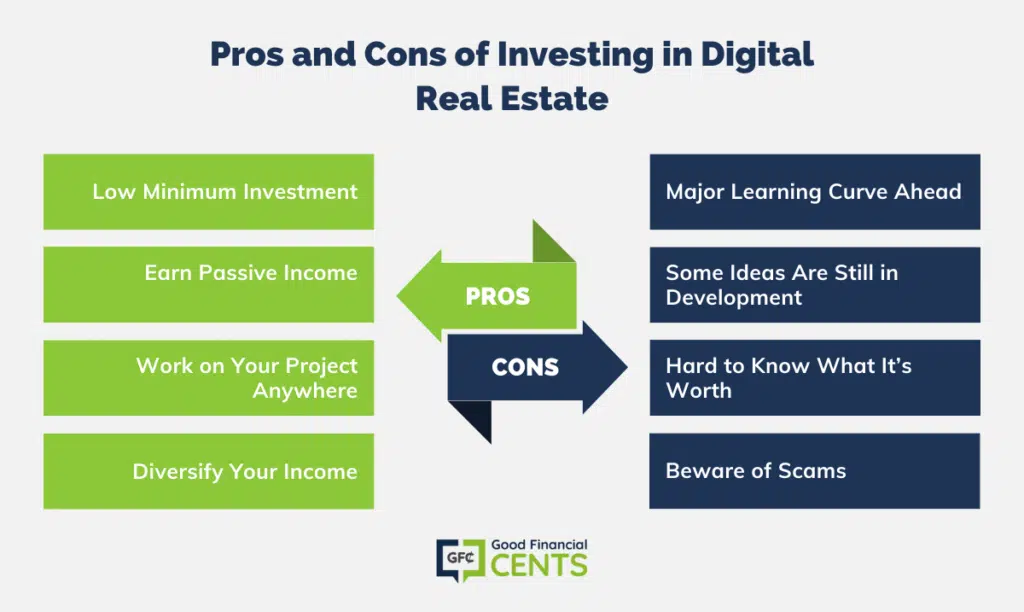

Pros of Investing in Digital Real Estate

- Low minimum investment: Where you’ll likely need tens of thousands of dollars to invest in physical real estate at a bare minimum, you can buy virtual real estate for a few hundred dollars or less. If you decide to build your own platform instead of buying one, your minimum investment can even be less than $100.

- Earn passive income: Digital real estate that is properly monetized lets you earn money when you sleep. This is especially true once you build up your platform so you have a ton of followers, and when you use a combination of affiliate marketing, ads, and sponsorships along the way.

- Work on your project anywhere: Building your brand can take place anywhere and at any time. All you need is a laptop and an internet connection to get started.

- Diversify your income: Finally, digital real estate can help you diversify your income in a major way. In addition to investing in stocks, ETFs, and other securities within a brokerage account, you can diversify with digital assets, too.

Cons of Investing in Digital Real Estate

- Major learning curve ahead: You will need to learn quite a bit about building online income streams before you can become successful. Also remember that, if it was easy, everyone would do it!

- Some ideas are still in development: Some digital real estate investment strategies are tricky to execute since they’re still being built. For example, it’s hard to know what you’re buying if you purchase land in the metaverse, or how you’ll make money with your investment.

- Hard to know what it’s worth: Digital real estate can also be difficult to price. For the most part, blogs, YouTube channels, and social media accounts are only worth what someone is willing to pay.

- Beware of scams: Finally, there are scams to watch out for any time a transfer of money or crypto may be involved. Make sure to watch out for investments that seem too good to be true, and conduct due diligence before you buy anything online.

The Bottom Line on Digital Real Estate Investing

Investing in digital real estate may seem scary, but there are plenty of ways to dip your toe in slowly and learn a ton along the way. The fact is, most people who wind up becoming successful online learn most of what they know through trial and error. That said, they had to get started first, and we all know that starting something from scratch can be an incredibly hard thing to do.

But, building wealth with digital real estate requires action, and sitting around thinking of ways to invest isn’t going to cut it. When it comes to investing in anything, be it digital real estate or the stock market, everyone has to start somewhere. So, figure out what you need to learn to get started, and don’t stop until you get where you want to be.