American Insurance Group, better known as AIG, is a leading global insurance organization.

AIG Companies provides a wide range of property-casualty, life insurance, retirement products, and other financial services to customers in more than 80 countries and jurisdictions. If you’re looking for an insurance product, there’s a good chance AIG companies will be able to help.

Table of Contents

AIG Life Insurance

The company has more than 46,600 employees who work across the globe. This international approach has been part of AIG’s business since 1919 when American businessman Cornelius Vander Starr founded the firm in Shanghai. In 2019, a century later, the insurance giant excels in offering flexible and affordable life insurance to customers worldwide.

In 2019, AIG’s revenues exceeded $49.75 billion.

Here’s another number that can help put AIG’s size into perspective: Over the last five years, more than $40 billion in claims and benefits have been paid out by AIG’s American General Life Companies.

The History of AIG

AIG got its start in Shanghai, China, in 1919 as a general insurance agency called American Asiatic Underwriters.

Within two years, the firm’s American founder, Cornelius Vander Starr, added a life insurance division and the business grew steadily. The company added branches in Southeast Asia throughout the 1920s.

In 1926, the company opened its first American office which did business as American International Underwriters Corp. From there, the company extended into Latin America.

In 1939, with World War II threatening the stability of markets throughout the world, the company’s headquarters moved from China to New York City.

The company’s expansion resumed after the war as the recovering economies of Japan and Western Europe offered new opportunities. In 1967, the firm combined its global operations into one firm, and the AIG name was born. Two years later, in 1969, the company went public.

Since then, AIG has added additional product lines, including transportation, energy, and entertainment holdings in order to serve the needs of various specialized industries.

The company emerged from the financial crisis of 2008-12 as a more efficient, streamlined organization, having re-paid government loans by selling some of its peripheral holdings.

To compare rates from AIG click here.

Products Offered by AIG Direct

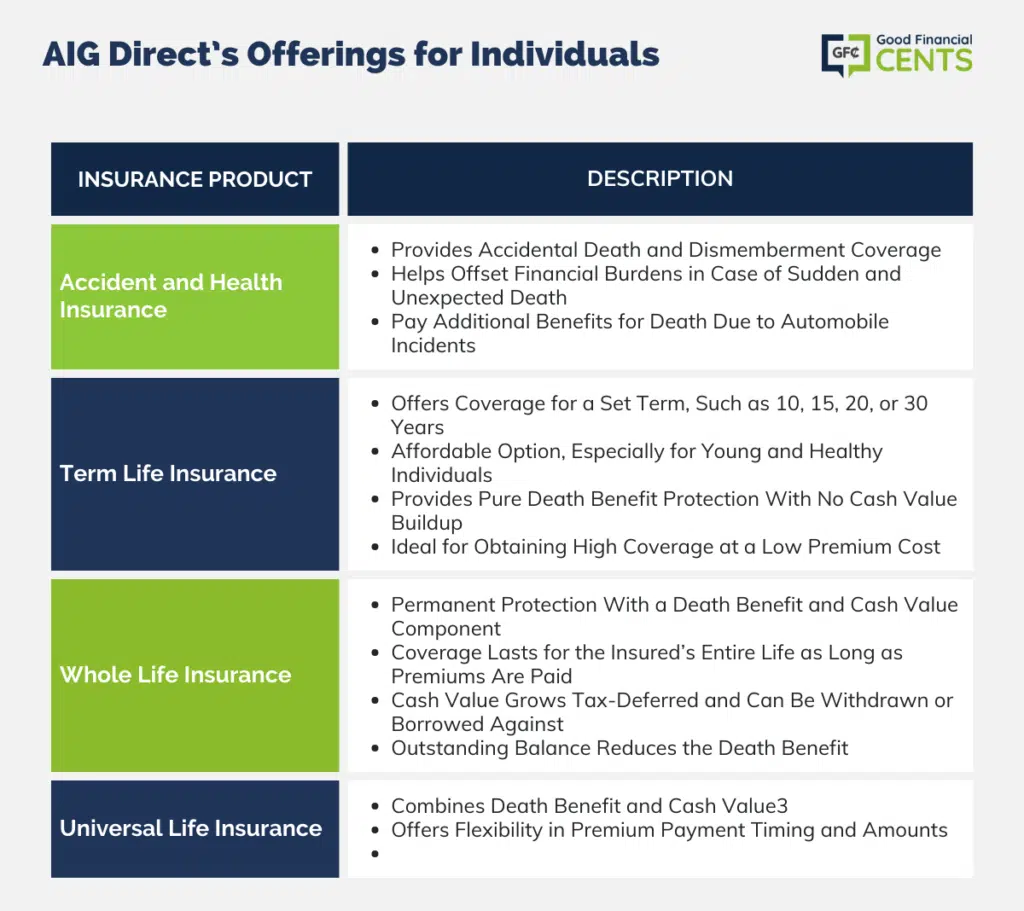

AIG Direct offers a wide range of products and services to both the individual and business markets. For individuals, AIG Direct’s offerings include:

- Accident and Health Insurance – Accidental death and dismemberment insurance can help offset the financial burden that is faced when a loved one passes away suddenly and unexpectedly in a disaster. This type of coverage will typically pay out an additional sum of money if the insured’s death is due to an automobile incident as opposed to sickness or other natural causes.

- Term Life Insurance – Term policies will cover an individual for a set amount of time, such as 10 years, 15 years, 20 years, or even 30 years. In most cases, term life insurance is very affordable coverage – especially if the insured is young and in relatively good health when applying for coverage.

This is because term life provides only pure death benefit protection, without any type of cash value build-up. Term life insurance can be a great way to obtain a high amount of coverage for a low premium cost.

- Whole Life Insurance – Whole life is a form of permanent protection. This type of coverage provides a death benefit, along with a cash value component. As its name implies, whole policies are designed to cover an insured for the “whole” of his or her life. This means that, as long as the premium is paid, the coverage will remain in force.

The monetary value that is associated with a whole life policy is permitted to increase on a tax-deferred foundation – meaning that there is no tax due on the gain until the time of withdrawal. This can essentially allow the money to accumulate and compound at an increasing rate over the course of time.

The whole policyholder is authorized to withdraw or borrow cash from the money value component for anything that he or she sees as okay. It is important to note, though, that any unpaid balance at the insured’s death will go against the amount of the death benefit that is given to the beneficiary.

- Universal Life Insurance – Universal life insurance allows policyholders both death benefit and cash value – however, these policies are much more flexible than whole life in that policyholders can choose when to pay their premiums, as well as how much to pay. (This can, however, affect the amount of the death benefit and value within the policy).

AIG’s Ratings

AIG holds high ratings from the insurance company rating agencies.

These include the following:

| Rating Agency | Rating | Description |

|---|---|---|

| Standard & Poor's | A+ | Strong |

| Moody's Investor Services | A2 | Stable |

| A.M. Best | A | Excellent |

| Fitch | A+ | Stable |

Ratings as of 5/4/18 Standard & Poor’s 21 ratings are a measure of claims-paying ability and range from AAA (Exceptionally Strong) to R (Regulatory Action). A.M. Best’s 15 ratings are a measure of claims-paying ability and range from A++ (Superior) to F (in Liquidation).

Ratings can be objective indicators of a company’s financial strength and can provide a relative measure to help investors select the best insurer for their needs. Ratings are subject to change at any time and are not a guarantee of the future financial strength and/or claims-paying ability of the company.

Note on variable annuities:

Better Business Bureau

While the rating agencies, above, look at a company’s internal financial health, the Better Business Bureau and other similar sources can give you an idea about how a company works with its customers.

The BBB has rated AIG A-, basing its rating on AIG’s commitment to resolving customer disputes. The BBB states that its ratings do not reflect an analysis of a company’s product quality, just its interaction with its clients.

Considering AIG Direct

AIG Direct offers a nice array of insurance products, and AIG has good ratings from the insurer ratings agencies. That means it should be a reliable partner for your long-term insurance needs.

But, as with any insurer, it’s important to consider your specific insurance needs and to find out whether AIG has a history of meeting the needs of clients whose applications may look similar to yours.

While all insurance companies’ underwriters seek to identify the risk an applicant poses, each company has a different approach, and, over time, these variances can turn into trends that we can monitor.

You may like AIG more if…

- You have recently lost weight

- You have been diagnosed with diabetes

- You like applying for insurance online

You may not like AIG as much if…

- Previous generations in your family died of heart disease or cancer

- You have high cholesterol

- Need a quick decision on your policy

For example, some companies look more favorably on people who are overweight or people who have type 2 diabetes.

In the case of AIG, we have noticed applicants who have some adverse health conditions find it harder to get approval. So, if your health history includes struggles with high cholesterol, for example, you may be frustrated with AIG’s response.

AIG also tends to emphasize an applicant’s family health history more than some of the other industry leaders.

If previous generations of your family struggled with heart disease or diabetes, AIG may be more likely to place your application into a higher-risk category, which means higher premiums if you get approved for coverage.

Since it can take weeks to go through the underwriting process, this can be frustrating, especially if you’ve taken the time to get a medical exam. If AIG tends to fall short in your specific area of need, you should keep looking.

On the flip side, if AIG does well in the areas where you need a little help, it’s well worth your time to apply.

If you’ve recently lost weight, for example, AIG may be more likely to classify you in a more favorable health category. The same goes for diabetes.

Lastly, AIG Life Insurance

To get the best coverage for your needs – regardless of your health condition – it is always best to make some comparisons.

Any time you are making a major purchase, you want to ensure that you’re getting the very best deal. You probably wouldn’t buy a car, or even an appliance, sight unseen.

Yet with life insurance, it’s harder to make comparisons because it’s a less tangible product. Once you’ve bought it, it’s easy to forget that your policy is in place.

But just like any other product, you’ll be depending on your purchase to do its job: to protect the people you love for decades, or perhaps for the rest of your life if you’re in the market for permanent life insurance coverage.

If AIG isn’t right, then we can direct you to other companies, like Banner.

It’s worth it to take your time and make sure you’re finding the right coverage, for the right amount of time, at the right price.

How We Review Insurance Companies:

Good Financial Cents systematically reviews U.S. insurance companies, emphasizing policy offerings, customer experiences, and overall reliability. Our goal is to present a balanced and comprehensive perspective to potential policyholders. Editorial transparency remains a cornerstone of our approach.

We actively collect information from insurance companies and place significant weight on customer feedback. By integrating this feedback with our research, we can offer a well-rounded evaluation. Each company is then rated based on multiple criteria, resulting in a star rating from one to five.

For a deeper understanding of the criteria we use to rate insurance companies and our evaluation approach, please refer to our editorial guidelines and full disclaimer.

AIG Life Review

Product Name: AIG Life

Product Description: AIG Life, a division of the multinational finance and insurance corporation AIG, offers a wide array of life insurance products tailored to individual and business needs. With a rich history and a global reach, AIG Life emphasizes flexible solutions, financial strength, and customer-centric service.

Summary of AIG Life

AIG Life, operating under the vast umbrella of American International Group, Inc. (AIG), has been a notable name in the life insurance sector for decades. Catering to diverse demographics, the company provides term life, whole life, universal life, and a variety of specialized insurance products, ensuring clients receive coverage best suited to their circumstances. With a commitment to innovation, AIG Life continually adapts its offerings to the evolving financial landscape and individual client requirements. Their deep industry knowledge, combined with a strong global network, positions them as a reliable choice for life insurance solutions.

-

Cost and Fees

-

Customer Service

-

User Experience

-

Product Offerings

Overall

Pros

- Diverse Product Range: AIG Life offers a comprehensive suite of life insurance products, allowing clients to find coverage that aligns with their specific needs.

- Global Presence: As part of the larger AIG network, AIG Life benefits from the corporation’s worldwide reach and expertise.

- Financial Stability: AIG, with its long-standing history, is known for its financial strength, giving policyholders confidence in the company’s claims-paying ability.

- Customized Solutions: The company emphasizes tailored insurance solutions, ensuring each policyholder’s unique needs are met.

Cons

- Complex Product Details: With such a vast product range, some consumers might find the variety overwhelming or the details intricate.

- Customer Service Variability: As with many large corporations, customer service experiences can vary, with some policyholders reporting delays or inefficiencies.

- Premium Pricing: Depending on the product and individual circumstances, some premiums might be higher than industry averages.

- Past Controversies: AIG, as a parent corporation, has faced controversies in the past, particularly during the 2008 financial crisis, which might concern some potential customers.

Worst insurance company don’t buy Aig. My mom passed away more than a year , I cancel my trip to Cancun and they not pay me yet. They close my case without let me know, then they reopen and never let me talk to the manager of the claim department. They let me wait, hang up on me and lied to me that someone will call back to me and never did. I call to them weekly and nobody care to listen to me they would hang it up and say someone will call you. Bad customer service so search for different insurance company and never buy Aig. Worst business. With the company like this it should close down.

If AIG is one of the better insurance companies, we are in serious trouble. They have horrible customer service and struggle to resolve problems. They are great for taking your money but do very poorly resolving problems/issues. If you need to call customer service, God help you!

information on an index annunity

Need information on Index annuity and what average yields expected

New Policy Holder And I’ve Been Having Trouble With My Policy Ever Since .I Signed Up Last Month. AIG Put What They Wanted On My Policy……

Worse insurance company to deal with, they will not be there for you when you need them the most

The info they give in this article is false. Their bbb rating if F

This company has been the worst to have to deal with your customer service people are horrible just trying to straighten out some information on for freaking policies that my mother had as she passed away having to deal with your customer service has been the worst experience ever in my life I would never recommend this company anything

Need life insurance quote for myself and my children