As someone who is economically active, filing your tax return is an activity that may seem daunting. Because of the costs involved, you may not view the services of a tax professional to be a viable option. You may also not have the confidence and experience to prepare and file your tax return yourself.

Tax software solves this problem for a lot of people. There are many products available to choose from, and you should consider your tax situation carefully before selecting the one that’s right for you.

This review takes an in-depth look at E-file, its features, versions, and some of the software’s benefits and drawbacks.

Despite being one of the lower-cost tax software solutions available, E-file is user-friendly and suitable for a wide range of tax situations.

Do not confuse E-file, the tax software we are reviewing today, with IRS e-filing, the general online tax filing process.

Table of Contents

Our E-File Review: Here’s How It Works

To prepare your tax return, E-file adopts an approach that combines the interview style with DIY facets.

The interface is straightforward and doesn’t feature all the bells and whistles that one can expect to find with some of the other top tax software interfaces.

When you prepare your return with an E-file, you have to complete several sections. There is, for example, one section for income, one section for expenses, and so forth.

Each section has its own subsections. Before you start completing a section, you have to answer some questions about your personal and financial situation.

After answering the questions, the software will guide you toward completing the relevant forms and schedules for your unique situation.

If you already know which forms apply to you, feel free to skip the interview at the beginning of each section.

Features

Pay with your Refund

If you use E-file for tax return preparation and filing, you can pay for their services with your tax refund.

The reason many people prefer to do so is that they don’t have to enter their credit card information and make an upfront payment.

Return Importing and Filing

If you are using E-file for the second year in a row, you can import your tax return from the prior year directly to the return of this year.

If you used the prep and filing services of a competitor platform, however, you will not be able to import your return, which is a feature that many other software solutions have available.

With E-file, you can also file returns from the previous year. If you didn’t file your return last year, you could do so at no additional costs.

Help Sidebar

E-file’s help sidebar is a helpful tool, especially for new tax filers. The sidebar provides tax information on the sections and subsections that you are currently working on.

This tool also directs you through the process of preparing and filing your return.

As you complete your information, the sidebar is automatically updated to provide you with information that is unique to your tax situation.

Audit Assistance

This high-value feature includes audit assistance at no additional costs.

E-File Plans

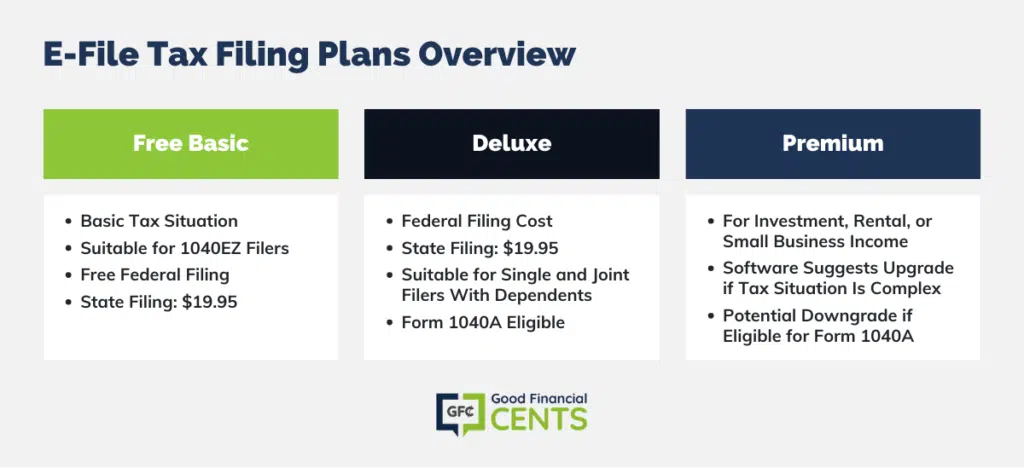

Free Basic

If you have a basic tax situation and you are free to file a 1040EZ, this version will be suitable for your tax preparation and filing. Federal tax filing is entirely free, and state tax filing has a service cost of $19.95.

If you select one of E-file’s paid plans and the software detects that you are eligible for the Free Basic plan, they will automatically downgrade your account and you won’t have to pay to file your return.

Unlike its competitors, E-file doesn’t charge you per state return.

Even if you have to file multiple returns, you will only have to pay the standard fee of $19.95. If you have to file in more than one state, E-file may, therefore, be the most affordable option for you.

Check out E-File’s Free Basic Filing>>

Deluxe

With the Deluxe plan, you will have to pay to file a federal return while the cost of state return filing is the same as the Free Basic version.

The Deluxe plan offers all the features that you receive with the Free Basic. Also, this version is suitable for single tax filers and joint filers who have dependents.

If you are eligible to file your taxes with Form 1040A, the Deluxe plan may also be your best option.

Premium

If you earn investment income, income from rental properties, or income from a small business, the Premium version from E-file can accommodate your tax situation.

If you selected the Deluxe version and the software picks up that your tax situation is moderate to complex, it will suggest that you upgrade to Premium version.

Likewise, if you purchased the Premium plan but you are, say, eligible to file with Form 1040A, the software will downgrade your account, and you will not have to pay the higher fee.

E-file Prices

The costs of state tax return filing are the same for all three plans.

Whether you have one or more state tax returns to file, you will also have to pay the standard fee, which is currently $19.95. The cost per federal tax return that is filed differs from plan to plan.

With the Free Basic plan, filing a federal tax return is completely free. If you selected the Deluxe plan, you would have to pay $24.95 per tax return.

Filing a federal return with the Premium plan costs $34.95 and, although this is the most expensive plan that this software has to offer, it is one of the most affordable programs available for people with complex tax situations.

The prices listed above are subject to change. To find out what the current fee of a plan is, head over to E-file’s website.

Bottom Line

E-file is an affordable, straightforward, and secure option for filers with both simple and complex tax issues.

Once you’ve worked with E-file once, the software becomes even more beneficial, allowing you to easily import last year’s returns.

Their audit support is also top of the line, ensuring you get the assistance you need when you’re facing an IRS audit.

Whatever your tax filing situation, E-file can help you to file without a headache and confusion this year.

You can also take a look at our federal income tax guide to help you along the way.

Start filing with E-file today>>

How We Review Tax Preparation Software:

Good Financial Cents reviews various tax preparation software options, emphasizing user experience, feature sets, and accuracy in calculations. We aim to provide users with a balanced perspective, assisting them during tax season. Our editorial process is transparent and thorough.

We source data from software providers, testing functionalities and evaluating user interfaces. This hands-on approach, combined with our research, ensures a comprehensive review. Each software option is then rated based on its strengths and weaknesses, resulting in a star rating from one to five.

For a deeper understanding of the criteria we use to rate tax preparation software and our evaluation approach, please refer to our editorial guidelines and full disclaimer.

Product Name: E-file Product Description: E-file is an online tax preparation and filing platform that allows users to easily navigate the complexities of tax returns. Designed for simplicity, eFile offers step-by-step guidance, ensuring that users receive the maximum possible refunds. Their system is ideal for those who prefer a straightforward and cost-effective solution to handle their tax needs. Summary of E-file Established as an alternative to traditional tax filing methods, eFile aims to demystify the often daunting process of preparing taxes for both individuals and businesses. By offering intuitive software that breaks down tax forms and terminology into easily digestible steps, eFile ensures that users understand every part of the filing process. Beyond basic tax preparation, the platform provides advanced tools, allowing users to factor in various deductions, credits, and specific financial scenarios. With a focus on user-friendly interfaces and comprehensive tax support, eFile has positioned itself as a reliable ally during tax season. Pros Cons

E-file Review

Overall